The Leg Unrun

This is the case against Ethereum's death, made at full strength. There's a static under the tape the obituary can't hear yet — light past the visible spectrum, and no one's pricing it.

$1,773.94. Roughly 64 percent below a high it touched exactly once, last August. The “ultrasound money” thesis is dead, the L2s ate the fee revenue, the Foundation is shrinking, ETH/BTC printed a fresh 2026 low last week — and your timeline is writing the obituary.

This week Bitcoin kept flushing — down hard through $62,700, the obituary’s best stretch in months, the kind of tape that’s supposed to bury a high-beta asset like ETH. So watch what ETH actually did underneath the headline. It made a higher high against Bitcoin and climbed for four sessions running off a higher low while BTC fell. Dominance fell with BTC instead of rising into the fear. The alts are four billion dollars larger in aggregate than they were before the dump. Hold both at once: the absolute price is still pinned near its lows, and the relative strength is real underneath it. Those two facts coexist — the obituary reads the price and misses the picture.

This is not the first eulogy. Ethereum has been declared dead more than a hundred times — there’s a tracker that does nothing but count them: the 2018 collapse from $1,400 to under $100, the 2022 bust, the “Shanghai upgrade will kill it, every validator flees” panic that never came, the post-election wave in late 2024 when it sat flat while Solana and Bitcoin ran. Every one of those calls was wrong in the only sense the word dead actually means — ETH didn’t go to zero, the project didn’t die. (Which is not the same as saying it can’t draw down to a power-law low. It can. Not dead is not can’t fall.) But “it was wrong before” is exactly what the bagholder says at the top, so I’m not leaning on it. The four-year-cycle crowd has joined the funeral too, and theirs is the heaviest charge: not just that the alt leg should have fired by now, but that Bitcoin topped on schedule in October and the whole complex — ETH worst of all — is headed for a cycle-bottom bloodbath.

Rotation Compresses made the structural case and then refused to call the up-or-down — it left ETH’s leg cut short mid-run, its sequencing to an all-time high still ahead this year, and handed the resolution to a decision tree. This piece pays that debt, because the smartest bear on the timeline has a genuinely good argument right now — better than the screaming-obituary version — and it deserves to be made at full strength before it’s answered.

· · ·

The case, and the answer

I’ll be honest: ETH right now is an underdog story, and I’m a contrarian by nature — I hunt the nuance that could become the next narrative, get positioned while it’s still unloved, and trim into the crowd that shows up late. The bear’s case deserves better than the screaming version on your timeline, so I’m going to make it at full strength and answer it as I go. What I concede stays in plain view. Anyone who tells you this bear is stupid is selling you something.

Start with the rule this whole piece is named for: ETH’s leg comes after Bitcoin’s, and it hasn’t run yet. The bear’s version is sharp. The “ETH lags BTC” rule is really two data points — 2017 and April 2021 — and in November 2021 ETH topped the same day as Bitcoin, so a third of the sample doesn’t even fit. Grant the rule anyway and the lag was weeks, not the eight months since Bitcoin topped last October. Worse, the cleanest instrument says the rotation isn’t coming at all: ETH/BTC sits below its 200-week moving average, the textbook long-term relative bear market, and a rotation thesis requires that chart to turn first. It’s doing the opposite.

Three things are wrong with that, and the first matters most, because it’s where people misread what “the leg is unrun” even claims. The rule was never “ETH lags by a fixed number of weeks.” It is narrower and harder: ETH tops at or after Bitcoin and has never once topped before it. Against that claim the record is three for three, and the same-day November 2021 top confirms it rather than breaking it. This is a statement about sequence inside a run — ETH is the last car on the train — not a bet that a four-year clock is ticking. I think that clock is the weaker framework, and I’ll say why later. The sequencing is the durable pattern.

Second: a broken lag means ETH didn’t finish its leg on schedule. It does not mean the leg already happened — because ETH never printed a higher high than Bitcoin’s cycle high, which in all three prior cycles it eventually did. We are not eight months into an expired lag; we are in a state no prior cycle ever produced — BTC topped, ETH didn’t follow, and ETH never made its own high either. That is genuinely off-pattern, in a way that cuts at me as hard as it arms the bear. Unresolved either way. Anyone certain here is bluffing.

Third, the ratio is not at a multi-year low — the bear has the chart backwards. ETH/BTC bottomed at 0.01770 in April 2025, in the Liberation-Day tariff panic, then ran better than 130% to about 0.04324 by August on ETH’s $4,953 high, and sits near 0.0283 today — a higher low than the cycle trough. Made a low, more than doubled, held a higher low: that is the shape of a base, not a terminal decline. And it’s live — through this week’s flush, with Bitcoin breaking down hard, the ratio didn’t just hold; it ran. A falling ratio is the definition of “ETH hasn’t rotated yet,” not evidence it never will; every ETH leg in history began from a depressed, falling ratio, and the turn up is the confirmation, never the leading indicator. Pointing at a low ratio to argue against rotation is pointing at a low price to argue against a bottom. One concession lives in that chart, and the broken ETH burn — the value-capture critique I’ll come to last — is what forces it: this coil is building low, in the high-0.02s on top of a 0.02 floor, where prior cycles coiled nearer 0.05 and ran from there. The ceiling is lower than it used to be. So the question was never “back to 0.08” — it’s whether the next leg runs off a higher low, the way every prior one did.

The second argument is just the tape, and calling it special pleading is fair: a record liquidation interrupted the move. The October 10, 2025 deleveraging wiped out $19 billion and cut perpetual open interest 43% in a single session, and it hit everything — BTC down 14%, ETH down 12%, SOL down 40%. Singling that event out to explain why ETH specifically failed looks like special pleading, and the simple null — ETH topped at $4,953 because that was the top — fits every data point. I’ll grant it cleanly: “$4,953 was the top” is a defensible read my thesis has to hold as live. But it cuts both ways, and sharper on the other side. That null requires ETH topping below its prior-cycle high and before Bitcoin finished distributing — something no prior cycle ever did. Mine requires one thing already on the tape: the largest forced-deleveraging event in the asset class’s history, a six-sigma print, landing in the middle of the rotation. Someone needs a special story. The bear’s is “ETH broke its own multi-cycle pattern for no reason.” Mine is “a record liquidation interrupted the move.” I’d rather defend mine.

The third argument isn’t really about Ethereum at all — it’s about what ETH isn’t doing while the rest of the risk curve runs, and the opportunity cost is real. The Russell 2000 printed a fresh high on May 28 — 2,942.61, leading every major U.S. index on the year. Every regulated, beta-friendly AI vehicle is making highs while ETH sits about 64% below its August peak. Why hold a low-velocity settlement asset compounding nothing when the same risk budget in equities compounds 20-40% with cleaner accounting and no on-chain tail risk? And the one vehicle built to carry ETH is leaking — spot-ETF outflow weeks, ETH leading every digital-asset fund in redemptions over one stretch. The opportunity cost is real. If you held ETH through 2025 into 2026, you paid for it. Concede it and move on.

The argument runs in one direction. Read it forward and it inverts. The bear is asking ETH to carve a fresh cycle low into a business-cycle expansion, into a Copper/Gold breakout that historically front-runs risk-on, into parabolic equities with the Russell leading every index, into Bitcoin dominance rolling over. Every prior ETH capitulation low — 2018, March 2020, 2022 — happened into a deteriorating tape. A capitulation low into a tape like this one would be an unprecedented divergence, and divergences resolve toward the dominant trend, not away from it. The risk curve climbs one rung at a time (the case I made in Rotation Compresses); the Russell at highs is the next rung firing, not the rotation skipping crypto. As for the outflows — net selling at maximum bearishness is the precondition for a rotation, not the verdict on it. The empty parking lot before the show, not the show cancelled. You don’t get the asymmetry without the empty lot first.

The fourth argument is the heaviest, and the one I respect most: the four-year cycle held last time because a cohort made it hold — so the bottom is ahead, not behind. This isn’t a chart squiggle; it’s a structural thesis with a perfect timing record. Bitcoin topped on October 6, 2025 at $126,198 — dead on the four-year schedule. Year two after the halving is the bear year. Every prior bear drew down 77-85% from the high, and the current low is only about 41-52% below the October top — so if the cycle is intact, the bottom is far below here, not behind us. ETH runs roughly 2.5x beta to Bitcoin on the way down, so it doesn’t run a leg; it bleeds to a cycle low. And this isn’t only the bear’s framework — my own catalog puts sub-$10K Bitcoin on the table and a 50-60% reversion. I don’t get to ignore it. Positioning agrees the top is in: CME ETH large specs sit at the 100th percentile of net-long, the most crowded long in the contract’s history, with Shapiro’s Crowded Market Report flagging ETH as a short setup. When the crowd is this long, you fade it.

I won’t pretend this one is refuted. On the tape, the bear is right, and I can see it. But it’s an argument, not a verdict — and the tell is why the cycle worked last time. The people who sold $126K down through $70K weren’t the COT’s large specs. (Those are Bitcoin levels — ETH has no separate clock here; it rode the same tape down at higher beta, which is the entire point.) They were the OG whales, the decade-long holders who finally watched a six-figure target print and took the exit they’d earned. Their selling manufactured a cycle-shaped top. That proves the cohort is influential. It does not prove the cycle is a law of physics — and this is exactly why I rate the four-year clock below the business cycle as a framework: a self-fulfilling prophecy holds only as long as the cohort that fulfills it still controls the float. That float is being absorbed, in measurable real-time size, by institutions and treasuries who have never traded the cycle and don’t believe in it. CryptoQuant’s CEO argues outright that diversified liquidity and long-term treasury holders have broken the old whale-sell, retail-dump rhythm.

And the positioning the bear leans on reads backwards once you account for who is actually long. Shapiro flags the short setup, then spends fourteen pages arguing against acting on his own signal, because the macro regime overrides it. In CME ETH, the commercial short is dominated by basis-trade desks and ETF authorized participants running long-spot against short-futures — not a directional bet — so “specs crowded long, fade it” may simply mean ETF basis demand is at record size, which is bullish: institutional cash queued to buy spot. The cohort that actually tops markets has already left — the same May 31 release puts small specs, retail, at the 0th percentile, fully flushed. The crowded side of this book is institutions, not the public. It’s the same handoff you can watch playing out in the float.

Which leaves the hardest, most concrete charge for last — the one the bear is right about: the value-capture mechanism is broken. Before March 2024, ETH was net-deflationary: EIP-1559 burned base fees faster than proof-of-stake issued new coin. Then Dencun gave the L2s cheap blob space, their fees fell 90-95%, and the burn went with them — in the 150 days after the upgrade, only 1,389 ETH burned from blobs, the blob base fee sat near 1 wei, and after Pectra the daily burn fell to about 3.26 ETH a day. Supply crossed back to mild inflation. The cut is surgical: the network succeeds, and the token doesn’t capture it. Everything in that paragraph is true, and I concede it on the merits — Dencun collapsed the burn, supply is mildly inflating, the L2s keep the sequencer economics. This is the real wound. But the bear’s claim is static — the mechanism is broken, full stop — and mine is a derivative claim: the mechanism is being rebuilt, with a moat poured underneath it, and the thing that actually sets price was never issuance in the first place. It’s float, and float is locking. Where the bear wins outright: if Fusaka’s fee floor doesn’t bite, if the volume never fills the blobs, and if formal verification never reaches production at scale, he takes this point. It is one of the two genuine risks in this piece — the other is the cycle clock. So it’s worth slowing down on, because it’s also where the answer is strongest.

· · ·

The tokenomics are being rebuilt

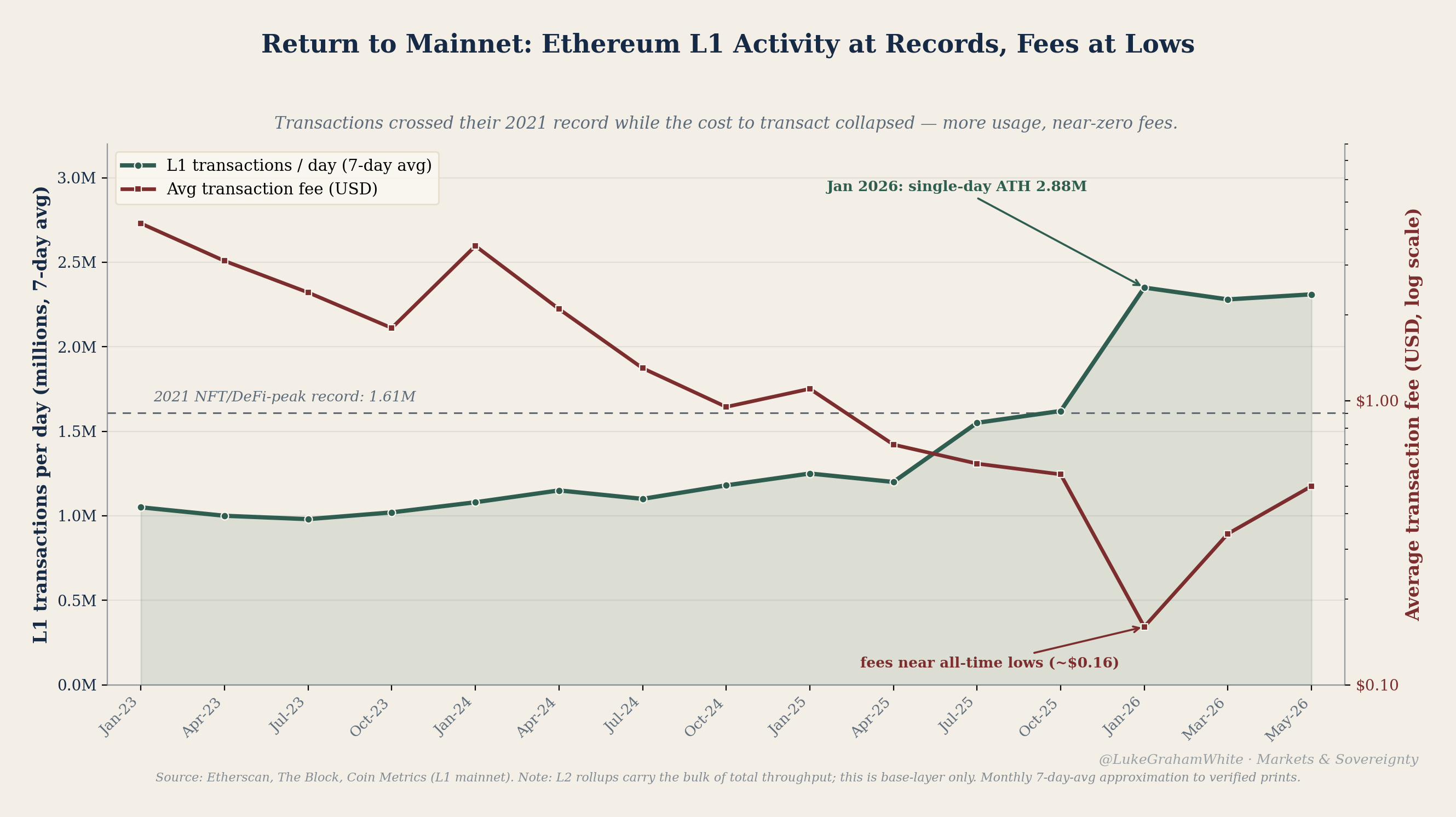

The system is reconfiguring in direct response to the critique. Fusaka activated December 3, 2025, shipping EIP-7918 — a floor under blob fees tied to L1 execution gas cost, roughly the base fee divided by sixteen. Before it, 93% of 2025 days saw blob fees at effectively zero. (Plain English: the developers fixed it. Blob fees can no longer collapse to nothing; they are tied to the regular gas price, so even quiet L2s still pay, and that still burns. Not a promise, a floor written into the code.) Fidelity Digital Assets modeled the fee floor since Dencun at an additional 24,641 ETH, about $78.6M, of cumulative revenue. And it is already in the data — per January 2026 on-chain analysis, ETH returned to micro-deflationary even at low activity post-Fusaka, with daily burn outpacing the 0.8% annual inflation rate. Fusaka also shipped PeerDAS and Blob-Parameter-Only forks — (Plain English: nodes now share the work of verifying data so the chain can carry far more L2 traffic, and capacity dials let developers raise throughput between upgrades) — moving the blob target from 3 to 14, max 21. The next fork, Glamsterdam, targeting June 2026, brings parallel execution, with a stated target near 10,000 transactions per second against 15-30 today. (Plain English: a 300-to-700-fold throughput increase attempted in one upgrade. It ships and the value-capture critique gets buried under volume, or it slips and the timeline is right. The market hasn’t priced either outcome.)

The logic is the only logic that ever made this asset work: you don’t get rich charging a high price for scarce blockspace; you get rich charging near-zero for an enormous and growing volume of it. (Plain English: the old model charged $50 a car and let through 100; the new one charges five cents and lets through a million. The Visa model, not the boutique hotel.) The base layer’s transaction count crossed its 2021 NFT-and-DeFi-peak record in late 2025 and printed an all-time single-day high near 2.88 million transactions in mid-January 2026 — while the average fee to transact sat near all-time lows, around $0.16. Activity has stayed elevated since, roughly 2.3 million a day through late May, well above the multi-year baseline. The crossover is the whole story: usage at record highs, cost to use it at record lows.

Return to Mainnet — Ethereum L1 transactions crossed their 2021 record while fees collapsed (Markets & Sovereignty; data: Etherscan, The Block, Coin Metrics)

One honest caveat the chart names: this is base-layer activity, and the L2 rollups now carry the bulk of total throughput — which is exactly the bear’s value-capture point, and exactly why the Fusaka fee floor matters, because it routes a slice of all that L2 volume back into the burn.

And there’s a moat almost nobody is pricing: formal verification. A security audit is humans trying hard to break the code and not managing to — useful, but probabilistic. Formal verification is a mathematical proof that the code does what it claims under every possible input, the way a geometric theorem is proven; once verified, that whole class of bug is simply gone. EF-funded work at Verifereum is shipping formal semantics for Vyper — grant FY25-1892, several compiler-pass proofs complete. To a treasury or a sovereign allocator, “the auditors checked it” and “mathematically proven correct” are different underwriting categories — and as AI-assisted exploit discovery accelerates, Ethereum being the chain where formally verified contract infrastructure ships first is exactly the value capture the bear says is missing.

Then the supply side, where the bear audits the wrong ledger entirely. The whole burn debate is about issuance — but issuance doesn’t set price. Float does. Roughly 30% of all ETH is staked, an all-time high, and it is locking rather than unlocking: the validator entry queue is the largest since 2023, the exit queue near zero. Spot ETFs and treasuries hold another 10-11% between them — BlackRock’s ETHA around 2.4%, BMNR around 4.5%, though most of BMNR’s stake sits inside that 30% rather than on top of it. Even netting the overlap, tradeable float is a shrinking minority — and the crowd is busy counting how fast water drips in while the reservoir drains into a vault. This has never been true before: 2017 had no staking, 2021 had tiny one-way-locked staking and no ETFs or treasuries. 2026 is the first cycle with all three locks running at scale during a demand vacuum — the maximum-asymmetry setup. The honest objection is that this lock, unlike Bitcoin’s lost coins, is reversible: stakers can exit, and ETF money is leaving right now. True — but the exit queue is slow by design, staking flow is still net inbound, and treasury holders are the stickiest hands the asset has ever had. Not Bitcoin-grade permanence. But tightening, not loosening. And that float is bolted to real demand: ETH carries 52.3% of DeFi TVL, 51% of stablecoin transfers at $3 trillion monthly, 54% of stablecoin market cap, 53% of tokenized assets, 65% of transactions (TrustShift, May 2026).

Those numbers settle a question the burn debate keeps dodging. Every blow-off in The Anatomy of a Blow-Off Top left the same wreckage: the technology was real, the infrastructure survived, the speculative flagship died. RCA ran two-hundred-fold into 1929, fell 98%, and never came back; the internet lived, most dot-com flagships didn’t. The tell for which side an asset lands on was always whether it captured recurring economic activity or only speculative flow. ETH captures the former — which puts it on the survivor side and recasts the whole charge: the question was never does ETH burn enough, it’s does ETH sit under real recurring activity. It does. The strongest version of the bear’s objection survives even that, and it’s worth stating: infrastructure surviving doesn’t force the token to appreciate — TCP/IP is critical infrastructure you can’t buy, and most ISP stocks never paid a dime. The difference is that ETH, unlike TCP/IP, is required to use the rails — gas, staking, collateral. A toll on the road, not just the road.

Finally, the treasury bid the bear said didn’t exist twelve months ago. Read it right — this is not one DAT versus another. MSTR is a Bitcoin reserve vehicle, a savings instrument; BMNR is an Ethereum yield vehicle on rails being tokenized in real time. Different addressable markets. BitMine (NYSE: BMNR) holds 5,416,901 ETH as of May 31, 2026 — 4.49% of supply, $11.6 billion — with 87% staked through MAVAN at a 2.73% yield, projecting $258-296 million in annual staking revenue. (Plain English: staked ETH pays yield in ETH, like a Treasury bond paid by the chain. MicroStrategy holds Bitcoin and earns nothing on it; BitMine earns a quarter-billion a year on top of the exposure, a treasury vehicle with a real income statement.) The validation just landed: FTSE Russell placed BMNR on the preliminary Russell 1000 list and SharpLink (SBET) on the Russell 2000/3000, effective June 29, 2026, with roughly $12.2 trillion benchmarked against the Russell indexes — at the exact moment the bear argues the institutional vehicle is broken. (On SBET’s share-accretion math, see our DAT mNAV Grid piece.)

That is the answer to the value-capture critique in full: the burn broke, and the system started rebuilding the capture mechanism the same quarter — while the thing that actually sets price, float, locked into the tightest configuration in the asset’s history, under real recurring demand, with a treasury bid that didn’t exist a year ago. Static critique, derivative reality.

· · ·

What actually moves regimes

Sentiment is loud in both directions right now, and sentiment is noise. Regimes don’t turn when the mood shifts — they turn when specific high-record signals fire, the ones with a perfect or near-perfect historical record. Several are firing or turning at once:

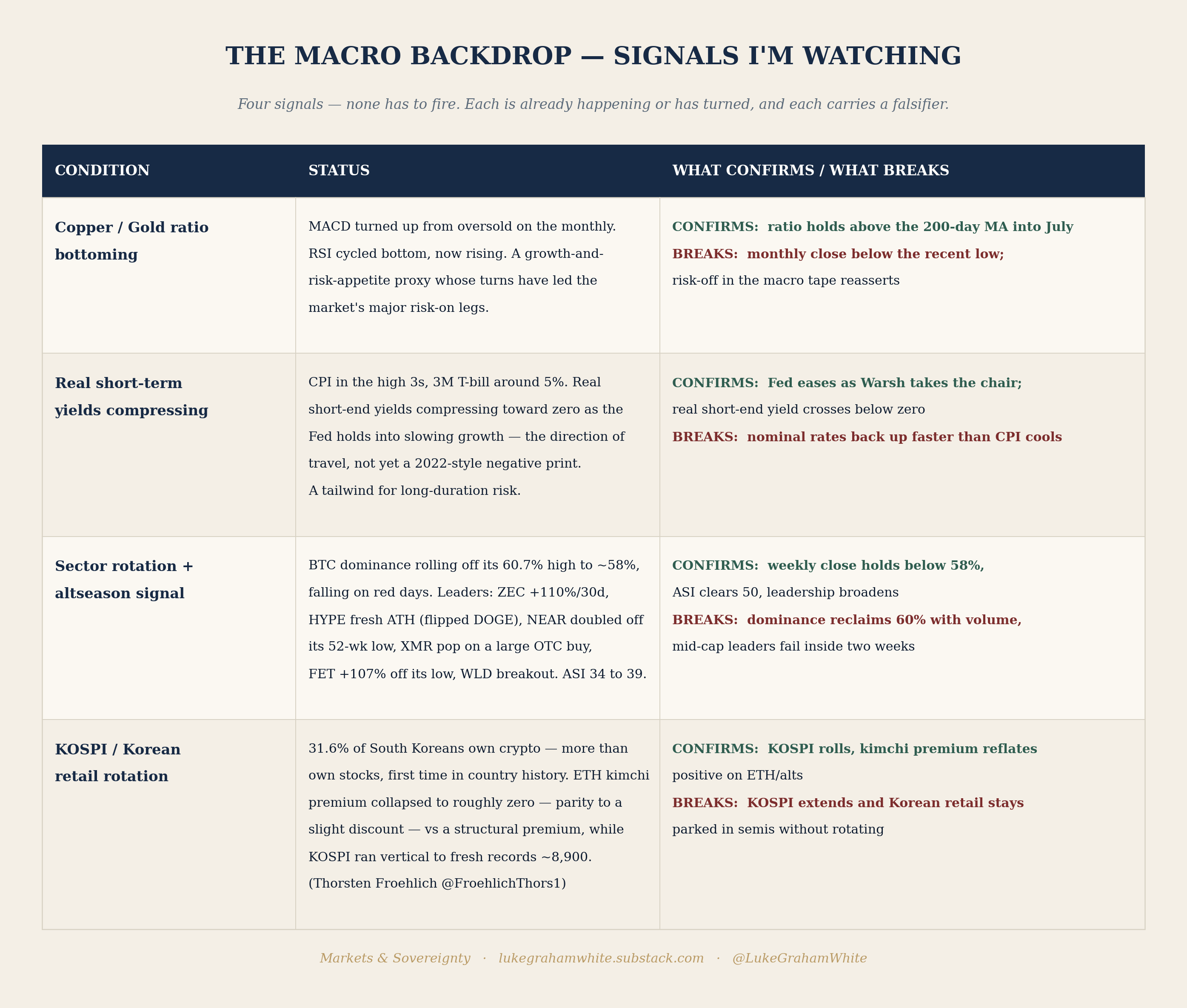

· The Copper/Gold ratio bottomed and turned up from a multi-year low — a growth-and-risk-appetite proxy whose turns have led the market’s major risk-on legs.

· Real 3-month yields are compressing toward negative on the short end as the Fed holds rates into slowing growth — a documented tailwind for the longest-duration risk assets, which is what crypto is.

· Bitcoin dominance is breaking down on red days — the one signal a rotation cannot happen without.

· The Global Liquidity Index — the multi-year cycle that has led every major crypto leg — is in an upswing.

The detail and the falsifier for each sit in the signals table further down. One more deserves its own look, because it is the one the bear has to explain away.

There’s a live tell the bear has to account for: every prior four-year bear shares one fingerprint — as BTC falls, dominance rises, ETH/BTC falls, and OTHERS falls hardest. This week, through a hard BTC flush, the tape is the exact inverse — a combination Sykodelic (@Sykodelic_) notes has never appeared inside a window where Bitcoin goes on to make new cycle lows. That’s a tell, not a verdict: one session’s relative strength is a necessary-but-not-sufficient condition, and a bear market’s fingerprint shows up over weeks, not hours. The absence of the fingerprint counts against the bear; it doesn’t close the case for the bull. The cycle bear is reading the calendar; the calendar’s own signature is missing from the tape. The triggers that would prove me wrong still stand — BTC losing the support band with conviction, the absorption channels stalling while aged supply keeps surfacing, the rotation reads rolling over — and if they fire, the cycle is intact and I’m wrong this year. By December I’ll either be vindicated or concede it cleanly; no hedging past then. (Note the reflexivity the bear’s own logic forces: if the cycle was self-fulfilling on the way up, breaking it is itself a violent parabolic catalyst, because everyone positioned for the cyclical bottom is offside.)

And the fifth: where the whole speculative complex sits in the cycle, measured by OTHERS — the total market cap of every coin outside the top ten. Here is the concept before the chart. Strip out Bitcoin and Ethereum and you are left with the pure speculative tail of crypto, and that tail behaves differently at the start of an alt season than at the end of one. At a launch it is coiled and under-owned, sitting quietly while the business cycle is still expanding. At a top it is stretched and over-owned, distributing into euphoria. Those are two visually distinct configurations, and the bear is pattern-matching this market to the second one — the mid-2018 and mid-2022 tops. The data says it is sitting in the first. Plot OTHERS and its dominance against a business-cycle reading running at 54.0 — solid expansion territory — and the speculative complex is parked at the same coordinates it held at the launch of the 2017 and 2021 alt seasons, not the distribution tops the bear keeps reaching for. It is the opposite of late-cycle. Sykodelic (@Sykodelic_) has done the cleanest chart work mapping this, and he paired it with a tape read worth quoting directly:

“Altcoins are actually $4bn higher in market cap after today’s Bitcoin puke. And dominance is down almost 1%. What we are observing here is an exhausted market in which alts are no longer responding to weakness. Bitcoin is actually being weaker than OTHERS.”

OTHERS and the business cycle — sitting at the same configuration as the 2017 and 2021 launch coordinates, not the late-cycle tops (chart: Sykodelic, @Sykodelic_)

Alts gaining ground on a BTC red day is the structural definition of rotation: the dominant asset losing ground to the cohort that’s supposed to drag behind it flips the standard relationship. Chart geometry plus tape behavior, pointing the same way.

That’s five signals — several with near-perfect records — firing or turning at once. The bear is reading the mood. The instruments are reading the regime, and the regime is turning over. Sentiment lags. Signals lead.

· · ·

The macro backdrop — where the money goes

Here is the only question that matters for a rotation: when the broad market pulls back — and the cycle work says mid-June into July — where does the money go? Answer it correctly and the ETH leg stops being a hope and becomes a position in a sequence.

Start with the sequence itself, because it is the spine that The Anatomy of a Blow-Off Top and Rotation Compresses were both building toward.

Foreign markets top first. It is one of the most reliable features of a major top: the speculative edges crack before the center. In 2000 the Nasdaq’s reversal showed up first in Tokyo, Seoul, and Frankfurt’s startup markets; in 2021 the periphery — ARKK, Chinese tech, emerging markets — peaked in February, while the big U.S. index kept melting up and hid the damage until the following January. The reason is simple: the riskiest, furthest-out stuff is the last money in and the first money out, and a firming dollar hits foreign markets twice — once in their stocks, once in their currency. That is the staircase from Rotation Compresses, and I won’t re-run it here. The one line to carry: the furthest-out things top first, and capital walks back down the stairs one step at a time.

That also answers why this rotation feels invisible: a rotation is a breadth event, an index is a cap-weighted average, and you can’t see the first in the second. The 2021 periphery top hid behind an S&P that melted up for eleven more months; the crypto rotation now hides behind Bitcoin dominance and a total-market-cap line the majors dominate. Breadth sees it. The headline can’t.

Which is why the KOSPI read is the signal I’d put at the top of the watch list right now — and why I’m going to spend real time on it.

South Korea is not just a foreign market. It is the single most concentrated, highest-amplitude, most retail-driven major equity market on earth, with a half-century record of being the most extreme expression of every global mania. In 1999 the KOSDAQ was the most violent retail blow-off of the entire dot-com era. The KOSPI’s strongest year since that 1999 peak was 2025, when it ran +75% — running at its dot-com-year pace again — and it is up roughly 100% year-to-date in 2026 on top of that. When a market reprises its dot-com-year performance two years running, the analog isn’t subtle.

But here is the piece most people miss: the KOSPI isn’t an independent signal — it is a levered derivative of the same trade driving the U.S. Samsung and SK Hynix are the physical memory-chip substrate of the entire AI buildout, so when Wall Street’s AI sentiment is euphoric, Seoul amplifies it. Korea is the highest-beta, highest-concentration pure play on the exact AI-capex thesis holding up the S&P — which makes it a far purer early-warning instrument than an unrelated periphery market. When the AI leg cracks, Korea cracks first and hardest.

Now look at the internals, because they are a textbook blow-off signature pulled straight from Anatomy:

· Samsung and SK Hynix together now make up roughly half the entire KOSPI — close to 48%, two memory-chip names. In Anatomy I wrote that past 40% concentration an index quietly stops being an index and becomes a leveraged bet on a handful of names. Korea has blown clean through that line. The KOSPI is now a leveraged long on the AI memory cycle wearing the costume of a national benchmark.

· The breadth underneath is collapsing as the index melts up. On the session the KOSPI broke 8,400, only 77 stocks rose against 826 declining — the exact late-stage divergence Anatomy names, advances concentrating into fewer and fewer names as the last holdouts capitulate into the leaders.

· The VKOSPI — Korea’s fear index — spiked into the low 70s while the index sat at all-time highs. A fear gauge at crisis levels during a melt-up is the signature of a market that knows, internally, how fragile its own ascent has become.

And there’s a mechanism wired straight into the top of this thing. On May 27, 2026 Korea launched sixteen single-stock 2x leveraged ETFs on Samsung and SK Hynix — over $6.7 billion in volume on day one. Leveraged ETFs rebalance daily in the same direction as price: on the way up they are rocket fuel; on the way down they are a forced seller that must hit bids to hold their ratio, whatever the price. And it is already measurable — Barclays put rebalancing flow at roughly 17% of SK Hynix’s daily volume and 10% of Samsung’s during the May 15 selloff, before the sixteen new products piled on. The instrument that let Korean retail lever up at the top is the same one that will force the unwind.

And the index has shown its hand a different way than the bears expected — not by rolling over, but by going vertical. The KOSPI tagged 8,476 on May 29 and kept going, closing a fresh record 8,801 on June 2 with an intraday high near 8,934 — roughly 100% on the year, stacked on 2025’s +75%. That isn’t the stall; that is the blow-off’s final acceleration, the parabola steepening on the worst breadth of the run. The distribution is visible in the instruments themselves: the KOSPI is still printing record highs, but Thorsten Froehlich’s read of the domestic leveraged and non-leveraged ETFs shows the late-blow-off signature — price gone vertical while net-buying intensity fades, cumulative volume delta making lower highs into a price that has nearly doubled. The parabola is running on less and less real buying. Distribution wearing the costume of new highs.

KODEX 200 (non-levered) — price at records while cumulative volume delta makes lower highs: net-buying intensity fading under a vertical price (chart: Thorsten Froehlich, @FroehlichThors1)

KODEX Leverage (2x) — the leveraged product where the most aggressive Korean retail sits, and where the forced-rebalancing accelerant lives (chart: Thorsten Froehlich, @FroehlichThors1)

Now the part that makes this an ETH signal and not just a Korea signal. AI/semiconductors and crypto are competing for the same marginal speculative dollar, and right now ETH is losing that competition decisively — which is why it feels dead. And you can see the drain in the cross-asset tape, not just infer it: Bitcoin has decoupled from the Global Liquidity Index it tracked for years, and from the software-equity complex (IGV) it moved in lockstep with — both climbing while BTC rolled over. Swissblock’s read of the flow is blunt: sell crypto to finance equity purchases. And nowhere is that migration more visible than Korea, where it’s the same retail pool — 31.6% of South Koreans now own crypto, more than own stocks for the first time in the nation’s history, the most momentum-chasing cohort on earth, and right now it is piled into KOSPI semiconductors instead.

The kimchi premium is the tell — and Thorsten Froehlich (@FroehlichThors1) was the first to map it cleanly against this rotation thesis. Korea’s capital controls trap crypto inside the country, so Korean prices normally sit above the global price — and that gap is the purest read of Korean retail demand there is. It has collapsed to roughly zero on ETH, dipping at times into a slight discount. For a market whose default is to pay up for crypto, parity-to-discount means one thing: Korean retail has stopped bidding ETH and started pulling money out of crypto and into the chip melt-up. The dead premium and the KOSPI concentration are the same flow seen from opposite ends — at maximum divergence. The spring is fully compressed.

Read the two together and the picture resolves into the single most important sentence in this piece: the thing starving ETH of capital right now is the thing whose exhaustion will feed it next. When the KOSPI concentration breaks — and a market that’s half two stocks, with breadth this rotten, a fear gauge this high, and a forced-selling mechanism strapped to the top, will break — that capital doesn’t evaporate. It gets freed, and the natural next home for exhausted hard-tech speculation is the other high-beta game in town: crypto. The kimchi premium reflating from today’s parity-to-discount back to a premium is the cleanest single confirmation the rotation has started — Korean retail coming home is the leading edge of the global pool doing the same.

One sequencing point, because it is where the argument could eat itself: today’s crypto flush is not that feed. Today is the drain — capital fleeing crypto into equities while the S&P sits at a record. The feed comes later, when the equity melt-up rolls over and that capital comes looking. Relative strength now is the leading indicator; the broad-market pullback is the trigger; the move is the lag after it. Don’t collapse the three into one event — the bear will, and call the drain the end.

From here the sequence is the one Rotation Compresses tracked: the blow-off tops in the periphery first (Korea), the broad market rolls, and capital walks down the risk-curve staircase. The pullback isn’t the thing to fear — it’s the entry. The flush is the setup.

The Thematic Run

The sector tape is already showing the early relative strength, sector by sector. A specific cohort is running, and the names tell you what the bid is about: Zcash +110% in 30 days (30% of supply now in shielded addresses, a record); Hyperliquid at a fresh ATH — $75.51 on June 2 — flipping DOGE out of the top 10; NEAR more than doubled off its 52-week low, with Grayscale and Bitwise both filing spot ETFs; Monero up double digits on a $23M OTC buy, after its first all-time high since 2018 (around $797) back in January; Humanity Protocol +750% off its YTD low; ASI Alliance (FET) +107% off its low. And Worldcoin (WLD) just broke $0.408 — its first 11-week high — with whale transactions, active addresses, and new wallet creation all printing 2026 records in a single 24-hour window. WLD’s AgentKit partnership with Coinbase-backed x402 (March 2026) makes it the cleanest single play on the AI-meets-identity primitive. Privacy as a sector gained 288% in 2025 — the best-performing crypto sector that year — and 80% of privacy tokens are up in 2026. The Altcoin Season Index has built from 34 to 39: early, selective relative strength concentrated in privacy, AI/identity, perp DEXs, and tokenized RWAs — not yet a broad rotation.

And here’s the escalation that lands hardest: it isn’t just thematic anymore — we’re also seeing culture and meme plays run. That’s a significant advancement on the purely thematic rotation theory: appetite has spread from use cases into the purely social. Over the past several weeks the meme complex has been among the loudest runners in crypto — MemeCore ran to a multi-billion-dollar cap and a near-$4.80 high; Pudgy Penguins, the dog (Dogwifhat) and the frog (Pepe) all put up double-digit weeks while the majors bled. Henrik Zeberg — who writes The Zeberg Letter — frames exactly this behavior as the disappearance of the fear of risk, and he has the historical rhyme for it: into the November-2024 top, Dogecoin out-ran Apple by more than 410% in twelve weeks. A joke beating the most valuable company on earth isn’t a market that has gotten smart; it is a market that has stopped being afraid. I’ll steel-man the obvious objection, because it’s the right one: memes ripping is the oldest late-cycle euphoria tell there is. Yes — and that is exactly what makes it a signal, not a coincidence. The casino turned its lights back on, and the first crowd through the door always heads for the loudest tables. Appetite that has spread from utility into culture is appetite that has stopped discriminating — the risk-curve clock ticking past the majors and the story stocks into the leveraged, the absurd, the purely social. It is the loudest tell on the board that appetite is reaching the end of the curve — the fingerprint that runs ahead of the move, not the move itself.

That cohort is not random. It is capital placing structural bets on where the next cycle of value capture lives — underwritten by the same macro forces driving the equity tape: SanDisk +600% YTD, Nasdaq and S&P at all-time highs, SpaceX, OpenAI, and Anthropic queued for IPOs at $1.78T, $1T, and $900B. Same script, same liquidity wave.

Why do these run before ETH, if ETH runs last? Because risk moves in two directions, and the order flips. On the way down, the highest-beta junk sells first, with crypto at the front of the forced-selling line. On the way up, the speculative edge leads early, because pricing a brand-new narrative is cheap and retail does it first, while the durable anchor is bid later and lasts longer, since institutional money is large, slow, and can only fit in the anchor. Down: furthest-out first. Up: edge first, anchor last. ETH is the anchor.

That two-directional risk curve isn’t only mine. Henrik Zeberg has built his macro framework around the same staircase, run the full length of it: blue chips, then small caps, then Bitcoin, then alts, and the meme tail at the very end. His canvas is the whole curve. Mine is one bead on it — ETH, the rung that runs last and hasn’t run yet. The one place we part is in method: he reads the staircase through Elliott Wave structure; I read it through cycle timing. Different instruments, same sequence. Where that matters: he holds the move runs on sentiment rather than a schedule, and I’ve laid a hard calendar over it — which means if the dates slip, his read survives mine doesn’t.

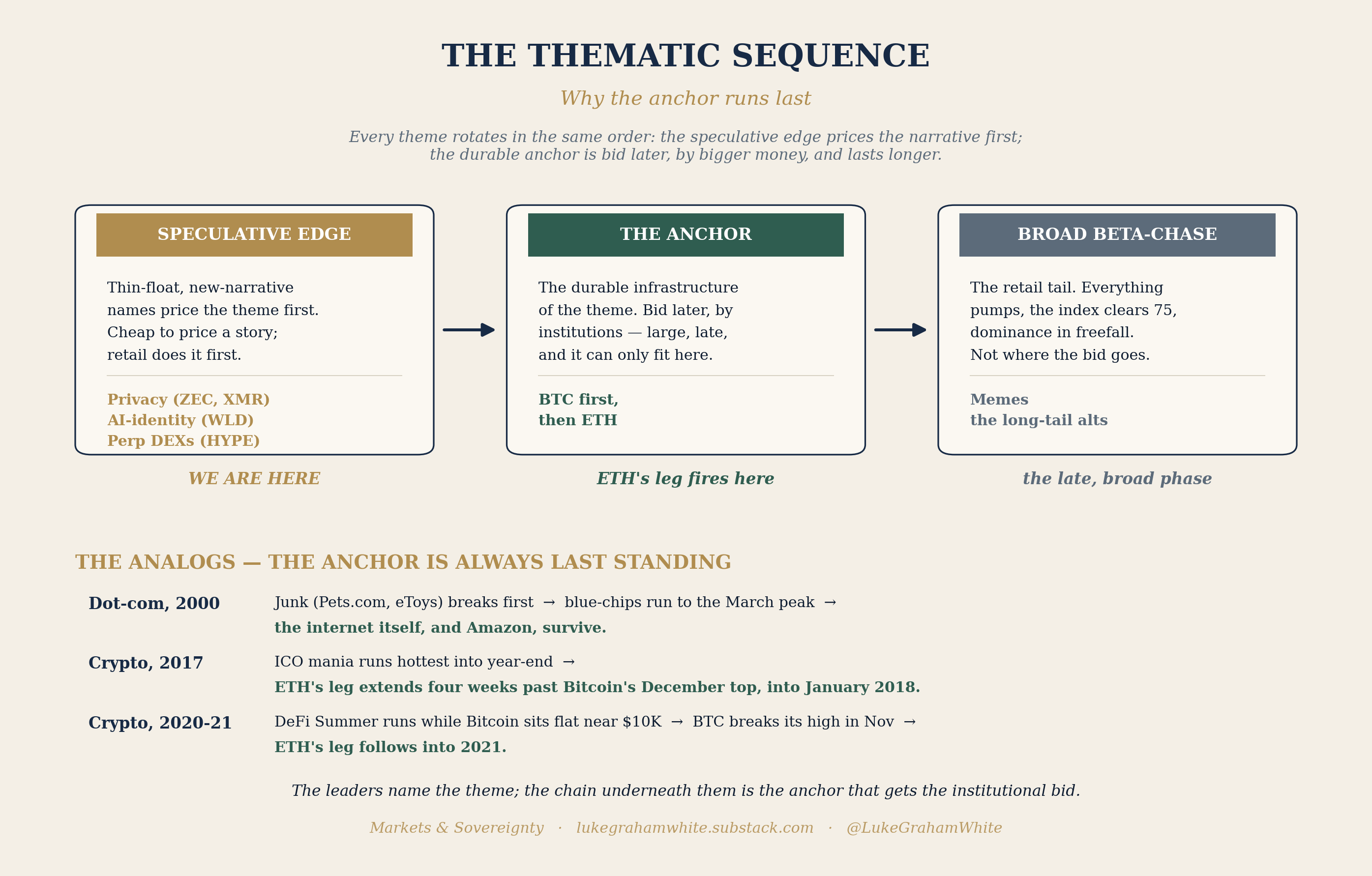

This within-theme ordering is the load-bearing shape in the whole piece, and it is a well-worn one. The speculative edge prices the narrative first, in whatever thin-float vehicle moves; the durable anchor — the infrastructure the theme is actually about — is bid later, by bigger and slower money, and is the thing left standing when the speculative names roll. It has happened in every theme that ever ran:

The thematic sequence — why the anchor runs last, with the dot-com, 2017, and 2020-21 analogs (Markets & Sovereignty)

· Energy, 1970s. The decade’s defining theme, oil and energy, ran to a record near 35% of the S&P by 1981, led the entire market, and then was the worst trade of the decade that followed. The hottest expression of a theme is the one that breaks hardest when the theme rotates.

· Dot-com, 2000 — the structural twin. The early-running names weren’t just “the riskiest” — they were bound by a narrative, the “.com” tag (a measurably distinct cohort: roughly 0.60% median daily return versus 0.05% for non-internet names). Within the theme the tops staggered by tier: the speculative junk (Pets.com, eToys) broke first, the blue-chips ran to the March peak, and the infrastructure — the internet itself, survivors like Amazon — was last standing and became the next cycle’s foundation. Junk first, quality next, infrastructure survives.

Map that onto now and ETH’s position is plain: it is the durable anchor of the crypto theme — the infrastructure, not the speculative edge — so it runs after the thin-float alts, and it is the expression most likely left standing when the institutional bid arrives. The alts running today aren’t competing with ETH for the bid; they are the speculative edge leading the anchor. Crypto has run this twice: in 2017 the ICO mania ran hottest into the end and ETH’s leg extended four weeks past Bitcoin’s December top into January 2018; in 2020, DeFi Summer ran while Bitcoin sat flat near $10,000, then cooled, capital rotated up, BTC broke its high in November, and ETH’s leg followed into 2021. Zeberg’s own record of that 2021 turn is the cleanest version of the pattern: the Nasdaq topped about ten weeks before Bitcoin, then tacked on only another 6-7% — while Bitcoin ran roughly 80% and ETH ran roughly 130%. The anchor goes last, and when it goes, it goes hardest.

And the forecastable tell the dot-com and energy analogs both confirm: the sector that leads names the theme the next wave concentrates in. In 2020 it was DeFi; the 2021 blow-off was a DeFi-and-L1 story. Now the leaders are privacy, AI-identity, and on-chain finance — and Ethereum is the center of gravity for all three: Vitalik’s public focus through 2025-2026 has been privacy and shielded execution at the L1, most ZK research lives in its ecosystem, and it already carries the majority of DeFi, stablecoins, and tokenized assets. The market is pricing those themes through whatever thin-float vehicle moves — ZEC, WLD, Humanity, Monero — but the themes point at the chain underneath them. These alts are the leading edge of ETH’s own thesis being priced, in the cheap vehicles first.

The crypto sequence, then, runs: narrative ignition, then the majors (BTC, then ETH), then the broad beta-chase and memes. We’re in phase one. The beta-chase beyond ETH is the retail tail — higher-beta, but not where the institutional bid goes; that bid stops at ETH.

Beneath all of that, four signals I’m watching — none of them has to fire:

The Macro Backdrop — Signals I’m Watching

None of these has to happen. Each is a signal with a confirm and a falsifier — a framework, not a forecast. Three of four confirming holds the asymmetry and you size accordingly; three of four breaking, and the bear takes it. The signals tell you whether, not when.

The live structural read — spot levels, EMAs, the COT specifics, the ETH binary range — sits in a separate piece. This one is the foundational argument. That one is the instrument panel.

· · ·

The cycles are clear

I run a cycle model. I’m not going to show you its guts — the inputs are the edge, and an edge you publish is an edge you’ve retired. What I’ll give you is the direction and the shape, because that’s the part you can trade, and it hasn’t pointed this cleanly in a long time.

The shape: one more push higher, then a sharp correction, then a 1-2 strong legs up into the back half of the year. That’s the sequence. The cycle work says the correction is coming — and that is the catalyst that sets the ETH leg in motion.

Now lay the crypto rotation over that calendar — and be precise about the order of operations, because the gap between a tell and a trigger is the gap between early and wrong.

Start with what today is, and what it isn’t. The relative strength on this crypto flush — Ether holding against Bitcoin, dominance rolling instead of spiking into the fear, the edge and now the culture names green while the majors bleed — is a tell. It says the drain is exhausting and the asset is coiled. It is not rotation, and I won’t call it that. Rotation is capital moving into crypto, and the capital isn’t here — it’s still inside the equity melt-up. What you’re reading is the fingerprint, not the move.

Rotation needs a catalyst, and the catalyst is a major correction in equities. This is the part most people have backwards: they wait for crypto to bottom on its own. It doesn’t. The thing that frees the capital is the equity shakeout — coming this summer — because that is what breaks the crowded mega-cap trade and sends money down the risk curve hunting the next high-beta game. The correction isn’t the threat to the thesis. The correction is the thesis. No shakeout, no rotation.

Which makes depth the whole ballgame. A shallow drawdown — six to eight hundred S&P points, the rotation case — herds capital down the curve into crypto. A deep one, the top of that 8-15% band, doesn’t rotate; it flushes, and crypto goes to the front of the forced-selling line with everything else, deferring the move a year. Same catalyst, opposite outcome, decided by how far it cuts. And crypto won’t be spared on the way down — it dips with the correction before it turns; the relative strength now is the tell that it dips less and turns first. So the read that matters isn’t whether the correction comes — it’s how deep it goes. Watch it like a hawk in late June.

If it stays shallow, the sequence runs in order, the way it always has: Bitcoin leads off the correction low, and Ether — the leg this whole piece is about, the one that has never fired before Bitcoin and always after — runs into the fall, concurrent with equities grinding to new highs. The late-year melt-up and Ether’s unrun leg aren’t competing trades; they’re the same capital, sloshing.

So why now, and not a vague someday? Because the correction is coming — the cycle says so — and the tells are already firing ahead of it. You don’t chase the bounce, and you don’t call today’s relative strength “rotation.” You let the equity correction hand you the entry, watch the reads confirm into the low — dominance breaking under 58 and holding, the ratio turning up off its higher low, Korea finally cracking — and position for the leg on the other side. Structurally bull. Tactically patient. Direction and shape are what cycles give you. The reads tell you when the patience ends.

· · ·

Old Ironsides

In 1812 the young American republic had six frigates against the most powerful navy on earth — a rounding error against the Royal Navy’s hundreds of ships. One of those six, Constitution, was smaller than the ships of the line she would never dare meet, but built tougher than anything her size: three feet of live oak and white oak under the planking, copper fastenings forged by Paul Revere. When British eighteen-pounders bounced off her hull off Nova Scotia, a sailor shouted “Huzza! Her sides are made of iron!” The little American frigate beat Guerrière, then Java — the first time an American ship ever took down a Royal Navy vessel of near-equal size — and she is still afloat today, the oldest commissioned warship in the world. Built to endure rather than to be the biggest, the small ship outlasted the empire that wrote her off. (Ethereum, the scrappy thing the giants keep declaring dead, could do worse than Old Ironsides for a patron saint.)

There’s one more thing the bears are reading exactly backwards. On May 24, Vitalik Buterin published a post describing the Ethereum Foundation deliberately shrinking — to something like 0.16% of supply, an opinionated node sitting alongside other nodes rather than above them, refocused on censorship-resistance, privacy, and self-sovereignty over raw speed. Longevity over breadth. The captain didn’t strike the colors; he built a smaller, tougher ship — one made to outlast, not to dominate.

The timeline read it as surrender — the captain reducing sail, the founder stepping back. It has it backwards. The EF can shrink to a tiny, opinionated node because the institutional adoption layer is being built by someone else, in parallel, right now. BlackRock’s ETHA already holds roughly $5.5 billion in ETH. BlackRock has filed for ETHB, a staked-ETH ETF that distributes yield to shareholders, with a final SEC decision expected this year. Nasdaq is integrating tokenized assets onto its rails. JPMorgan is settling collateral on Ethereum infrastructure. The financial industrial complex is not asking ETH for permission to use it. It is building on it, because the rails are already laid and the alternatives are worse. Price is someone else’s job now — and at the rails-and-treasuries layer, they are damn good at it.

That parallel is the part the bears miss. The EF is sharpening the sovereignty layer at the protocol level — privacy, censorship-resistance, formal verification — while the institutions above pour capital into the same chain. Different agendas, opposite in spirit, riding the same rails: the sovereignty layer makes them harder to capture, the institutional layer harder to ignore, and both accrue to the same asset.

And the people who will actually drive ETH’s price are mostly the opposite of sovereign — some of the largest nation-state-scale capital pools on earth, adopting this infrastructure because it’s the cheapest, fastest, most programmable settlement layer they’ve ever had. That points at the sharpest reason ETH is mispriced. Most assets have one buyer base — Bitcoin’s reserve buyer, an alt’s speculator. ETH has two independent ones: the TradFi infrastructure buyer (BlackRock, the banks, the treasuries, accumulating yield-bearing rails) and the crypto-native rotation buyer (the kimchi pool, retail, chasing beta). They have never shown up at the same time. In 2021 the infrastructure buyer didn’t exist; today the rotation buyer is absent. The configuration where both arrive — against the tightest float in the asset’s history — has never happened. It’s assembling now.

This is the deeper answer to the obvious objection — if ETH is the infrastructure, why isn’t institutional money already here? The instinct is “the asset class is too small and too young.” That’s the symptom, not the cause. The real reason is that until right now there was no compliant door for institutional-sized capital to walk through. The marginal buyer is a pension, an endowment, an RIA, an insurance general account — and none of them could hold spot crypto on an exchange; mandate, custody, and fiduciary rules forbid it. For fifteen years ETH had institutional-grade fundamentals and retail-and-degen plumbing. The bid wasn’t missing because the name was small. It was missing because it had no door.

That door is being cut right now, in 2026 — the spot ETFs, the staked-ETH ETF, the treasuries, the Russell inclusion, JPMorgan settling on-chain, Nasdaq tokenizing. And the bigger move behind it isn’t a lock at all; it is an unlock, still on the horizon. A young asset class has no allocation category — pensions don’t buy names, they fill buckets, and crypto isn’t yet a sanctioned line in the model portfolio. The system that decides which buckets exist has a name: Aladdin, BlackRock’s risk platform, the plumbing underneath a large share of the world’s institutional money. The day crypto becomes a recognized line item inside systems like that one, the bid doesn’t trickle in — it gets switched on by default, across the whole opportunity set, at once. ETH doesn’t need that unlock to run this leg, but it is the largest door of all, and it’s the subject of the next piece.

That’s why this is an inflection, not a slope. A pension doesn’t ramp from 0.5% to 0.6% to 0.7%; it holds zero until the bucket, the benchmark, and the approved language exist, then deploys the whole target in a compressed window. Nothing, nothing, nothing, then everything — because the gate was never price or willingness, it was permission, and permission flips like a switch, not a dial. And here the sizes stop being abstract: global stocks and bonds are hundreds of trillions of dollars; all of crypto is a few trillion. A rounding error reallocated out of that ocean is a doubling in this pond. Run a step-function bid that size into a locking float and you don’t get orderly appreciation — you get a gap. The same illiquidity that makes ETH “too small to love” today is exactly what makes the move violent when it triggers.

The argument over whether Ethereum matters is finished. It won that one. Whether ETH the token pays you for being right — on a horizon you can survive — is the open question, and the two parts of it that should keep you honest are the same two I conceded: the value-capture critique and the cycle clock.

The leg is unrun. That’s not a promise it runs. It’s a refusal to call it dead while it’s still coiled. If it does run — if ETH prints a new all-time high inside this calendar year — ask yourself what the four-year-cyclists will say then. When the universe they built their thesis inside shatters, how bad does the FOMO get? That’s the asymmetric nuance. The trade that pays is the trade nobody’s positioned for.

Here is what I think is actually happening, underneath the flat price. Three changings of the guard, all at once, in the same eighteen months. The holders are changing — the decade-long OG whales who lived the four-year cycle, handing their coins to institutions and treasuries that don’t believe in it. The stewards are changing — the Foundation shrinking to a small, opinionated node because it no longer has to hold the thing up alone. And the technology is changing — the value-capture mechanism rebuilt under the asset in real time, Fusaka shipped, the next fork already coming. Three load-bearing pillars of the entire system, swapped out at once.

That is what an inflection feels like from the inside: rough and volatile, the old structure failing before the new one takes the load. The bear sees a flat price and a dead tape and calls it the trend. But the surface is the last thing to move; underneath it, the current has already turned.

“The world has changed. I see it in the water. I feel it in the Earth. I smell it in the air. Much that once was is lost, For none now live who remember it.” ― Galadriel - J.R.R. Tolkien

The four-year cycle was the old world. What’s being built now is the next one. The leg is unrun because the new world hasn’t printed yet. But the water has already turned, and the hair on my arms are standing up.

The leg is unrun. Look to it.

· · ·

This piece sits in sequence with Rotation Compresses (the framework and the decision tree) and The Long Forgetting (the surge clock underneath all of it). Not financial advice. Position sizing is mission critical. The asymmetry is only worth taking at a size that lets you be wrong. — Luke

Luke —

This is exceptional work. The October 10th deleveraging argument stopped me cold — I've been wrestling with the math on ETH's interrupted run and this piece handed me the framework I was missing. When you lay it out that cleanly — no prior cycle ever produced a BTC top without ETH making its own high, and a six-sigma forced-liquidation event landing in the middle of the rotation — the null hypothesis collapses. That's not a failed cycle. That's an interrupted one.

I've been working through a similar sequencing thesis with Henrik Zeberg, and your staircase framing — furthest-out first on the way down, anchor last on the way up — maps cleanly onto what we've been developing around the AI infrastructure rerating sequence. The KOSPI read is the one I'll be watching most closely. The kimchi premium as a real-time rotation tell is genuinely useful.

The three simultaneous changings of the guard at the close — holders, stewards, technology — is the most honest framing of this inflection I've read. That's the part that deserves a wider audience.

Thank you for making the bear case at full strength before answering it. That's the only version worth reading.

Mark

Your finest work yet, Luke - and on the 11th hour; what timing!