The Long Forgetting

Why every empire is sure it’s different. Why every empire is wrong. A roadmap through the end of the cycle, and the spring on the other side.

Humans are almost comically forgetful. Not in the sentimental sense — we remember our first loves and our worst embarrassments — but in the civilizational sense. The things that happened before we were paying attention feel unreal to us. The things that happened before we were born feel like myth. And the things that happened before our grandparents were born might as well have happened on another planet.

Psychologists call it recency bias. Whatever just happened feels enormous. Whatever happened a long time ago feels small, if we remember it at all. It’s why every market crash feels unprecedented, every political moment feels like the worst ever, every new technology feels like it changes everything forever. Our mental timeline is tiny. We are, each of us, a blip.

The cycle doesn’t run because the universe is cruel. It runs because forgetting is what we do.

The thing that hath been, it is that which shall be; and that which is done is that which shall be done: and there is no new thing under the sun. — Ecclesiastes 1:9

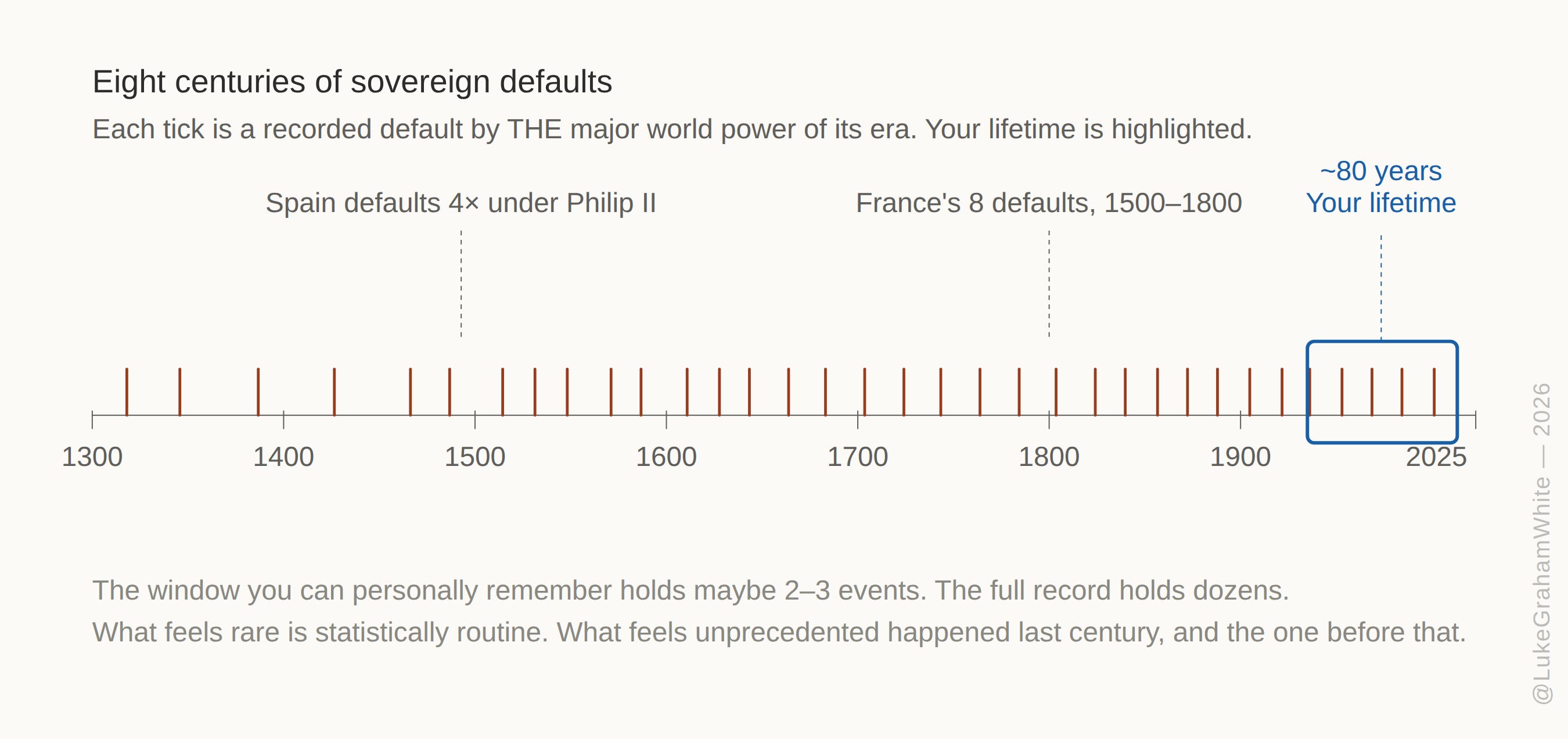

Each tick is a recorded sovereign default by THE major world power of its era. The rectangle is the window you can personally remember.

My crash course in finance began with a rekt portfolio in 2008. The thing that still gets me about it, all these years later, is that I hadn’t taken any risk. None. The account was being managed conservatively — supposedly — by a local banker at Chase. She was kind. She was reassuring. She wasn’t lying to me on purpose. She was just passing along the same story the entire system was telling itself, and the system was wrong. By the time the truth showed up in the numbers, the money was gone. That’s the lesson I took out of it and have held onto for twenty years: nobody is going to do this for you. Not the bank, not the advisor, not the system, not the people who seem like they know. Learn it yourself or get rekt by people who genuinely believed they were helping.

And looking back from here, every policy move since 2008 has the eerie quality of having been pre-ordained. TARP. ZIRP from 2008 to 2015 and again from 2020 to 2022. Three rounds of QE that took the Fed’s balance sheet from $900 billion to $4.5 trillion. Operation Twist. The Volcker Rule that wasn’t really enforced. Dodd-Frank’s stress tests, then the 2018 rollback that exempted the regional banks — including the ones that would fail in 2023. The 2019 repo blowup the Fed swore wasn’t QE while expanding the balance sheet by roughly $400 billion in five months. COVID’s $5 trillion in fiscal stimulus from March 2020 through March 2021, plus another $4.7 trillion in Fed balance sheet expansion over the following two years. PPP loans that ran straight to $200 billion of confirmed fraud, per the SBA’s own Inspector General. The 2023 banking scare and the BTFP backstop that valued underwater bonds at par — a one-year emergency that normalized the principle of marking-to-fantasy whenever the system needs it. The Treasury buyback program that launched in 2024 with $120 billion of annual capacity and was already expanded by 27% within a year. Every step looks, from any single moment, like a reasonable response to a one-off problem. Strung together, it looks like a script. I don’t think there was a master plan. I think there was a one-way set of incentives and a generation of policymakers who never saw a financial crisis they wouldn’t paper over. The result is the same either way.

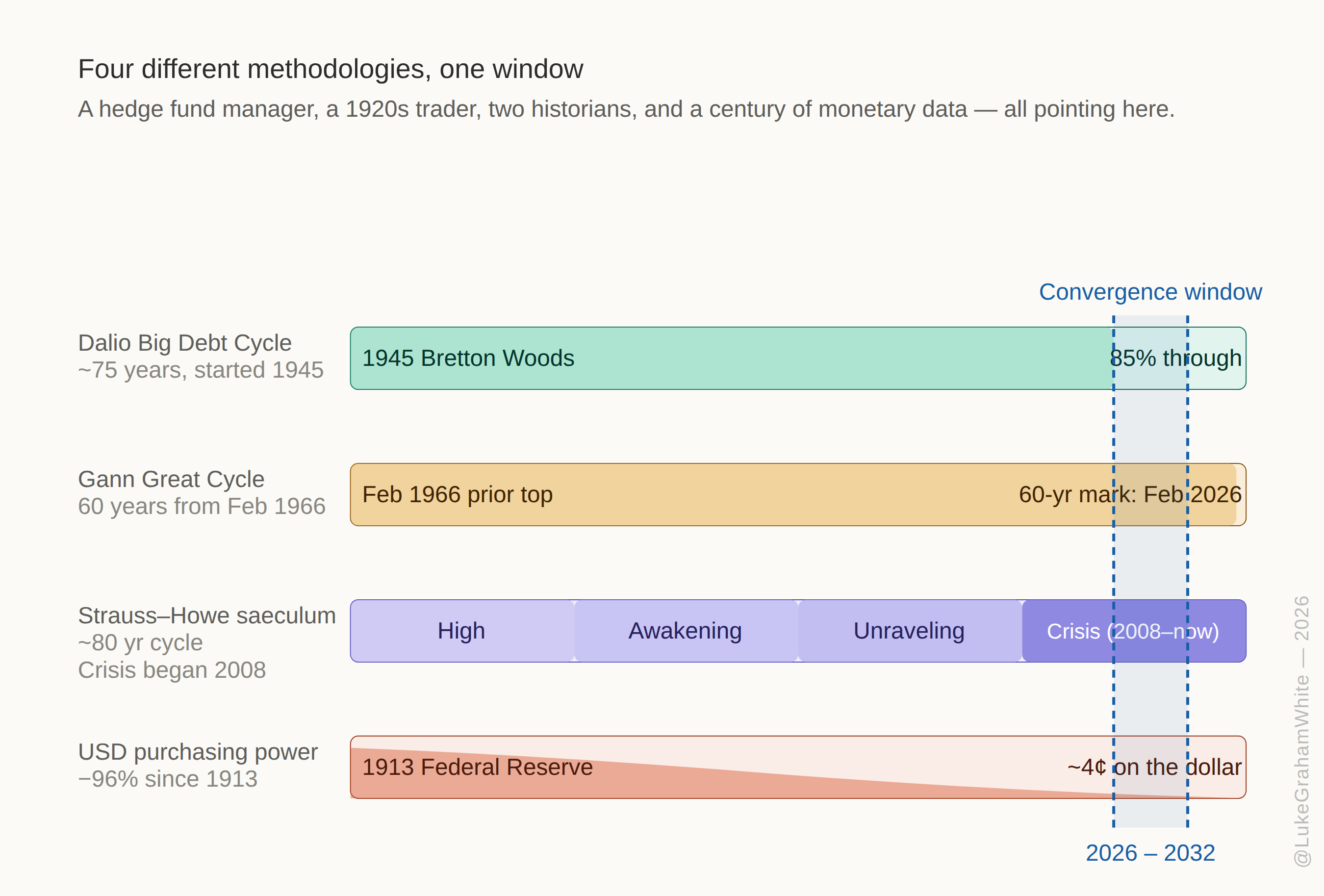

That’s the premise of this piece. What’s happening to the global economy, to the U.S. dollar, to the political order — none of it is new. It’s extremely probabilistic, extremely common, and the template is laid out clearly in the work of a few authors I want to walk through. Ray Dalio. W.D. Gann. Strauss and Howe. Carmen Reinhart and Kenneth Rogoff. Four very different disciplines, four different vocabularies, all pointing at the same door.

Four independent methodologies converging on the same late-2020s window.

Dalio’s Big Cycle: We’re in the Late Innings

Ray Dalio has spent his career betting on government debt. When he writes about how countries go broke, he isn’t theorizing — he’s describing the exact set-ups he trades against. His framework, laid out across Principles for Dealing with the Changing World Order and his newer book How Countries Go Broke, is deceptively simple.

Short-term debt cycles run about six years — your normal boom-bust where credit expands, asset prices climb, central banks tighten, things cool off, repeat. Most people recognize these because they’ve lived through several. Stacked on top is a much longer cycle, roughly 75 years give or take 25, which Dalio calls the Big Debt Cycle. The short cycles end because of rate mechanics. The long one ends because the debt burden itself becomes unpayable. Nobody alive has lived through a full one. That’s exactly why this moment feels unprecedented — because within your lifetime, it is.

By Dalio’s own reading, we are roughly 85% of the way through the current long-term debt cycle, which started in 1945 with Bretton Woods. The classic late-stage symptoms are everywhere: debts and debt service climbing faster than income, more supply of government bonds than natural demand, central banks forced to choose between letting rates rise (crushing borrowers) or printing money to buy the bonds themselves (crushing savers).

One person’s debts are another’s assets, and both must be satisfied. Late in the cycle, that balancing act becomes nearly impossible.

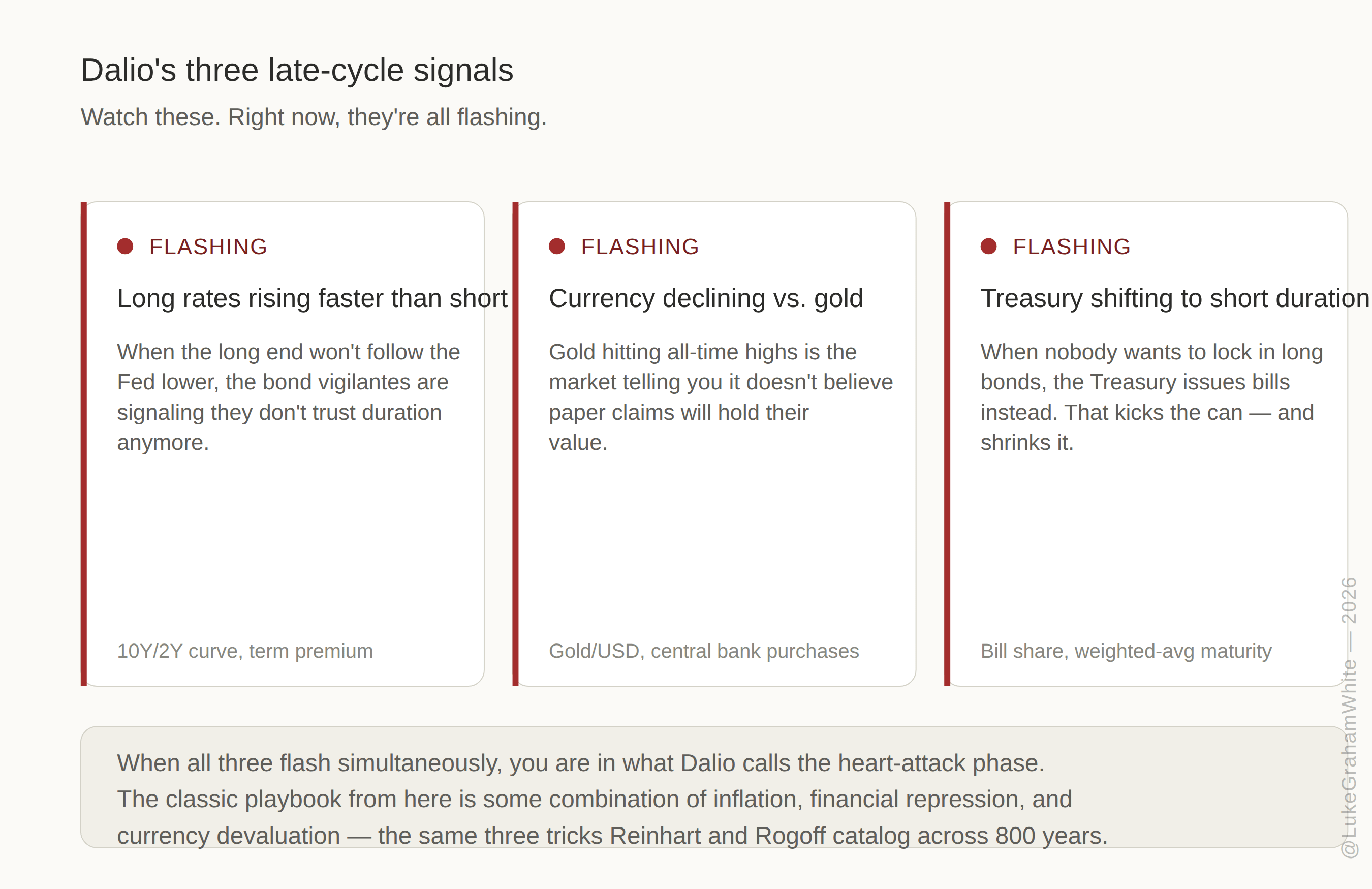

What follows is what Dalio calls an “economic heart attack” — a sudden seizing up of the circulatory system as debt-financed spending hits its limits. Three signals tell you it’s happening: long-term interest rates rising faster than short ones, the currency declining especially against gold, and the Treasury being forced to issue more and more short-term debt because nobody wants to lock in long duration. Watch those three. They’ve all started flashing.

The three indicators Dalio tracks. They are all currently flashing.

An Aside: This Isn’t Doomsday. It’s A Rebirth.

I want to pause here, because by now this piece has the gravitational pull of a tragedy, and I don’t want you to read the rest of it through that lens.

Bill Gurley was on Tom Bilyeu’s show recently and said something that stuck with me. He said he gets a little depressed every time he watches one of Dalio’s little movies — those animated shorts where Dalio walks through how empires rise and fall. I get it. The first time you really sit with the framework, it lands hard. The arc looks fixed. The conclusion looks foregone.

I respect Bill enormously. But there is something he is missing, and it’s the thing I want to put on the table here for anyone who’s ever closed one of these articles feeling worse than when they opened it.

This is not the end. It is the end of one cycle, and the beginning of the next. Every single Fourth Turning in recorded history has been followed by a High — a long, expansive, generationally optimistic period of rebuilding. The American Revolution was followed by the constitutional era. The Civil War was followed by the rise of America as an industrial power. The Depression and the Second World War were followed by the longest period of broadly shared prosperity in human history. Winters end. They always have. Being a student of history has actually taught me to be cautious, but optimistic here.

What’s happening now is not collapse. It’s molting. The post-1945 order — the dollar system, the central institutions, the centralized consensus — is what’s running out of runway. Not the country. Not the species. Not even the experiment.

Here’s where I think the standard “institutions die, new institutions are born” framing gets it wrong. What comes next isn’t more institutions. It’s more sovereignty and decentralization. The whole arc of the past five hundred years has been the concentration of power into central nodes — kings, nation-states, central banks, trans-national bureaucracies. This Fourth Turning is the inflection. The replacement is hard money and commodities you hold yourself. Productive land you control. Networks you can route around. Small-scale, sovereign, distributed.

And there’s a deeper cycle that rhymes with this one. The longest cycle anyone tracks — the 25,000-year precession of the equinoxes — is rolling us out of the Age of Pisces and into the Age of Aquarius. Pisces was the age of hierarchy and top-down faith, of central authorities and institutionalized belief. Aquarius is the age of the individual, of networks, of distributed knowledge and awakened consciousness. You don’t have to buy the astrology to notice the cycle. We are exiting a long period of consciousness held in place by central structures and entering one defined by the expansion of the mind itself. The monetary architecture is downstream of that.

That’s a rebirth, not a collapse. Painful, maybe. Disorienting, could be. But every previous Fourth Turning has resolved in the construction of a better order than the one that broke. This one might finally restore agency to the people who hold it instead of consolidating it further into hands that don’t.

Gann’s Master Cycle: The Trader Who Mapped Time

W.D. Gann was an American trader, born in 1878, who built his entire methodology on a premise most modern traders have forgotten: markets move in time cycles as much as price patterns, and the math underneath those cycles is the same math the universe runs on. The golden ratio. Fibonacci. The 360-degree circle. The harmonic intervals. Gann didn’t think he was mining mysticism. He thought he was reading the user manual. Markets, in his framework, are just one more expression of an intelligently designed clock — and once you know how the clock is built, you can read the time on it.

The track record is hard to dismiss. His most famous call was the 1929 crash. In November 1928, almost a year ahead, he published his annual forecast for the Dow. He pinpointed a sharp pullback in April, a resumption of the rally to a final top in early September, and then “the biggest crash in history.” The actual market top came on September 3, 1929. The crash followed weeks later. The 22-page forecast still exists; you can buy a reprint.

Gann identified a hierarchy of master time periods — 90, 60, 45, 30, 20, 10 years — and called the 60-year cycle the Great Cycle, “the greatest and most important of all.” Watch how it works. 1869: the post-Civil War speculative bubble ends in the Black Friday gold panic, the most violent market dislocation of the nineteenth century. Add 60 years. 1929: the greatest crash in history. Add another 60. 1989: the Nikkei tops at 38,915 on December 29, the peak of the largest financial bubble the world had ever seen, followed by a two-decade bear market that defined modern Japan. Three iron data points, sixty years apart, each one a generational market extreme.

Now add 60 to the next one. February 9, 1966: the Dow first touches 1,000 and then begins the sixteen-year secular bear that defined the boomer trading generation. The post-war Bretton Woods bull market had run out of road. The cracks in the gold-exchange standard were already visible. Five years later Nixon would close the gold window. February 1966 + 60 = February 2026. This year.

The 90-year cycle rhymes the same way. 1839 panic → 1929 crash → 2019-2020, where COVID broke the system and the Fed expanded its balance sheet by nearly $5 trillion in two years. Two independent cycles, two completely different anchors, both pointing at right now.

You can engage with Gann at whatever depth feels right. Skeptic? Take the empirical observation that markets repeat at fixed time intervals and use it. Believer? The geometry is there. Either way, you arrive at the same place the other three practitioners arrive at by completely different routes.

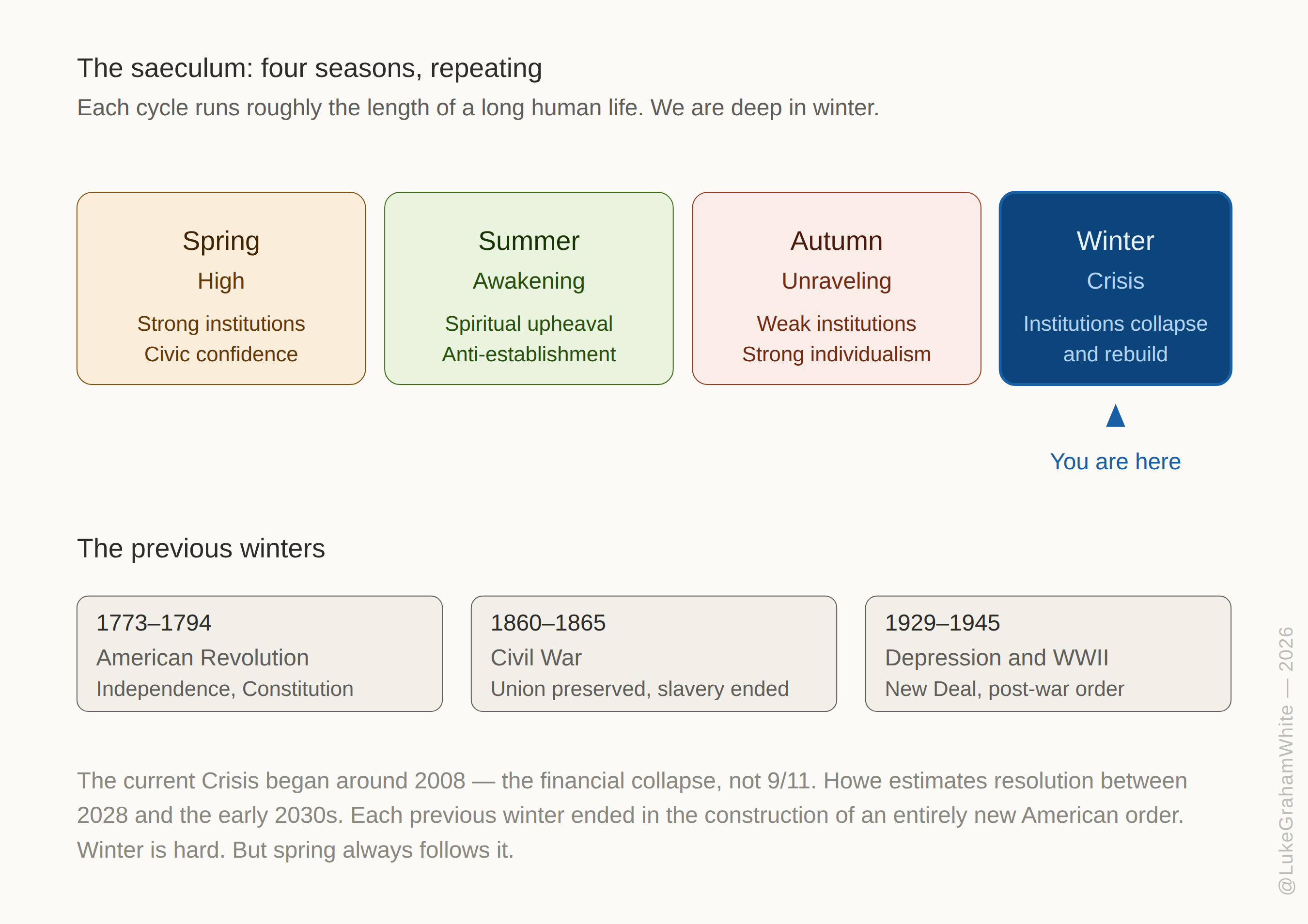

The Fourth Turning: A Cycle of Generations

William Strauss and Neil Howe published The Fourth Turning in 1997. Their argument is that Anglo-American history moves in 80-to-100-year cycles — roughly the length of a long human life — divided into four twenty-year seasons they call turnings. A High, then an Awakening, then an Unraveling, and finally a Crisis. Then it starts over.

The length matters. It’s the length of a long human life because that’s how long it takes for the generation that remembers the last crisis to die off. Once they’re gone, nobody alive remembers what it felt like. The lessons fade. The guardrails come down. And the cycle runs again. Forgetting is the engine of the whole thing.

The four seasons of the saeculum, with the previous American winters marked.

The Crisis is winter. It’s when the institutions built in the last High stop working, when old political coalitions fracture, when the country is forced to reinvent itself through hardship. The last Fourth Turning ran from roughly 1929 to 1945 — the Depression and World War II. The one before that was the Civil War. Before that, the American Revolution. Three Crises, roughly 80 years apart each time, each one unimaginable to the people living through the peaceful decades in between.

By their count, the current Fourth Turning began around 2008 — not 9/11, but the financial crisis. Which, if you’ll allow me a personal note, tracks with my own experience. That moment didn’t feel like the beginning of a twenty-year Crisis era. It felt like a one-off panic that would get resolved. In hindsight, it was the ignition. Howe’s 2023 follow-up, The Fourth Turning Is Here, argues we are now deep into the climax phase, with resolution likely sometime between 2028 and the early 2030s. The mood fits: distrust of institutions at generational highs, political polarization that feels pre-war, a pandemic, a banking scare, rising geopolitical conflict with near-peer rivals. None of that is random.

What I find striking isn’t that Strauss and Howe predicted any specific event. It’s that a historian working from generational patterns, a demographer looking at archetypes, and a hedge fund manager looking at sovereign balance sheets all arrive at the same window. The late 2020s into the early 2030s is when the old order has to either reform itself or be replaced.

Eight Centuries of Financial Folly

This Time Is Different: Eight Centuries of Financial Folly by Carmen Reinhart and Kenneth Rogoff is the definitive catalog of sovereign debt defaults across 800 years and 66 countries. The title is the punchline. Every generation, right before the crash, the experts explain why this time the old rules don’t apply. And every time, they do.

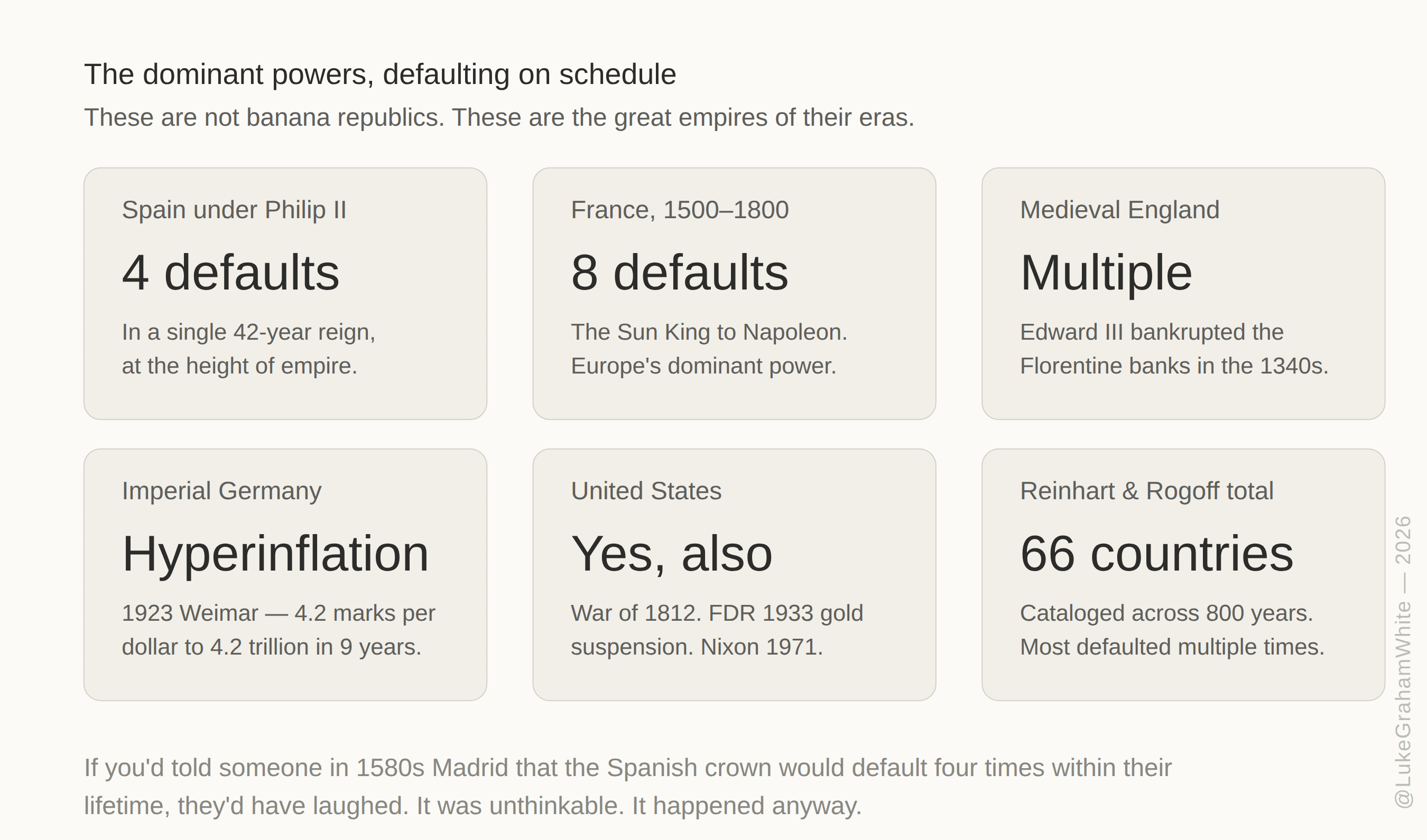

The Reinhart-Rogoff data is wild. Defaults are not rare events in the long view. They are the norm. Medieval England, then a rising power funded by Italian bankers, defaulted multiple times in the 1340s — and helped take down the Florentine super-companies that financed it. Philip II of Spain, at the height of Spanish global domination, with the silver of Potosí flowing into Seville and the largest empire the world had yet seen, defaulted four times during his reign alone. France, the dominant continental power of Europe under the Sun King and Napoleon, defaulted eight times between 1500 and 1800. Even the United States — which we tell ourselves has never defaulted — has done so multiple times, both implicitly (FDR’s 1933 suspension of the gold standard, which most economic historians count as default in substance even though the Supreme Court did not) and explicitly (War of 1812 debts the Treasury could not service, Nixon’s 1971 closure of the gold window).

The dominant powers of their eras, defaulting on schedule.

Let that list land. These were not banana republics. These were the world economies of their day. Spain at peak Habsburg dominion. France from Louis XIV through Napoleon. England at the height of medieval power and the dawn of the British financial revolution. Imperial Germany. The United States. Yes, the US has defaulted already. If you’d told someone living in 1580s Madrid — at the height of the Spanish Empire, with the New World’s silver pouring in and the Armada being prepared — that the Spanish crown would default four times within their lifetime, they would have laughed. It was unthinkable. It happened anyway. The exceptionalism people feel for their own empire, in their own century, is the same exceptionalism that has been felt by every empire and every century. And yet here we are, still doing the math.

Reinhart and Rogoff break down the mechanics. Sovereign defaults come in clusters, following waves of over-lending. They are almost always preceded by a period in which debt rises faster than income. And governments almost always try the same three tricks before formally defaulting: they inflate, they devalue, and they impose financial repression — forcing domestic banks to hold government debt at below-market yields. Only when those tools are exhausted do they renege outright.

Countries have at times escaped some of the real burden of their debt through inflation. This is not default in the usual sense because the debt is honored, albeit with currency of lesser real value.

Read that twice. The path of least political resistance — the one chosen again and again across centuries — is to pay the debt back with money that’s worth less. That is the template. And it’s the one the United States appears to be walking down right now.

So while it might feel a bit trite and super accurate to say that the US defaulting on its sovereign debt isn’t a big deal in the history of nations…I would definitely say, shit does happen.

Why Hard Money Matters: A Lesson from Ancient China

Here’s where the story gets interesting for anyone wondering why Bitcoin, gold, and other forms of “hard money” keep coming up in these conversations. The pattern in Reinhart and Rogoff’s data, and in Dalio’s cycles, isn’t random. Governments that can print their own money will eventually be tempted to print too much of it. Full stop. It’s happened in every single civilization that invented paper money. Every one.

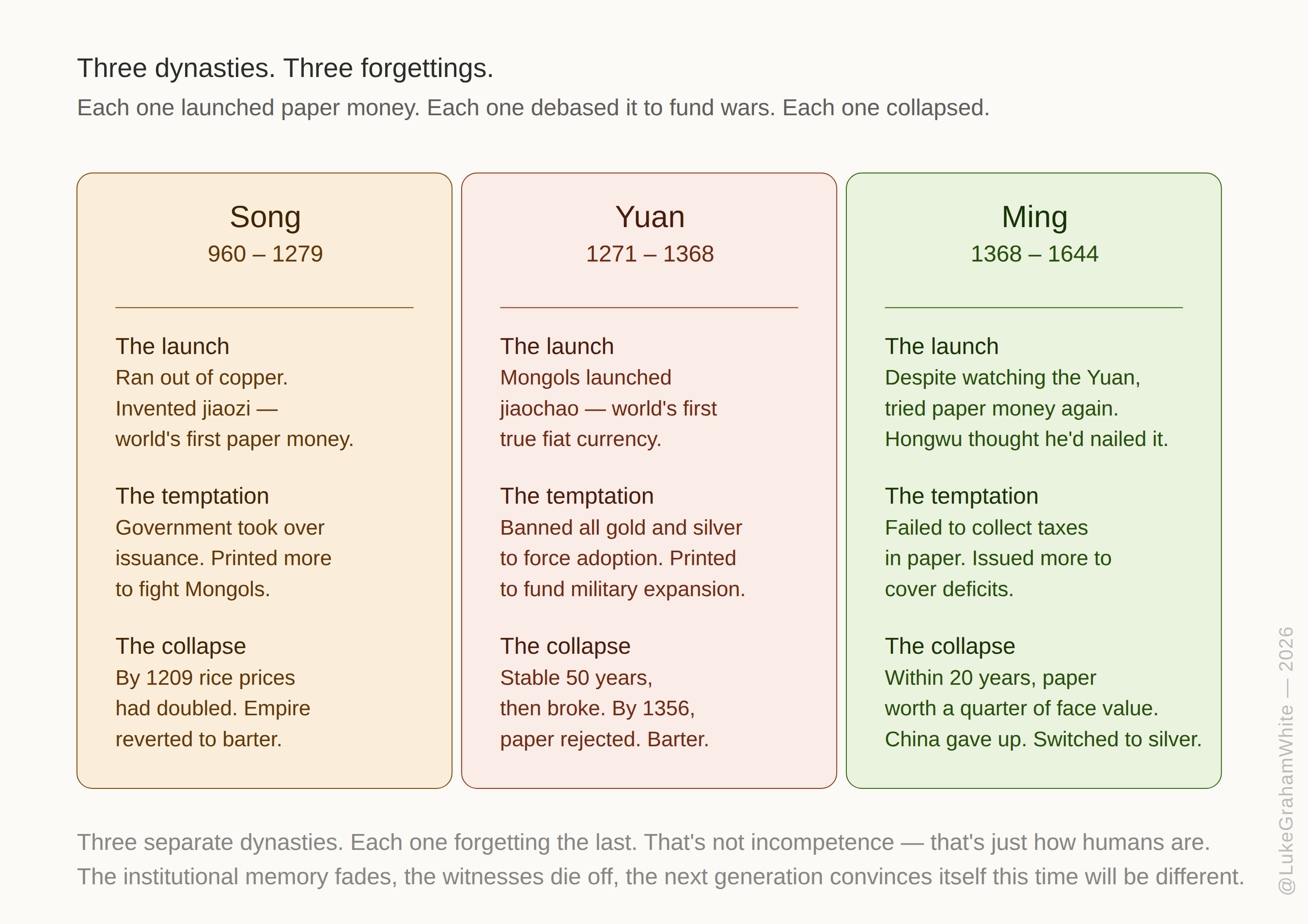

Ancient China is the original case study, and it’s instructive precisely because it’s so far outside our living memory that we can look at it without bias. The Song dynasty (960-1279) ran one of the most sophisticated economies in human history. The problem was that their economy grew faster than their copper supply. They literally did not have enough coin in circulation to lubricate commerce across an empire that size. So merchants in Sichuan invented paper money — jiaozi — as promissory notes backed by deposits of coin.

Three dynasties. Three identical paper-money collapses. Three forgettings.

At first it worked beautifully. The paper circulated at a premium to cash because it was easier to carry. Then the government took over the issuance. Then, facing the Jurchen and later the Mongol invasions, the government couldn’t resist printing more. By 1209, rice prices had doubled. By the time of the Southern Song collapse in 1279, the currency had been gravely devalued and the public was reaching for whatever metal coin or barter substitute they could find. The Mongols inherited an economy that had already been shown how to break paper money.

The Yuan dynasty that followed learned nothing. They ran paper money again. It collapsed again. The Ming tried it a third time in the 1300s and 1400s. Within decades of each launch, the paper was trading at a fraction of its face value. Eventually the Ming gave up entirely and China moved to a silver standard for the next five hundred years — not because silver was innovative, but because silver was the one thing the emperor couldn’t conjure out of thin air.

Three separate dynasties, each one forgetting the last. That’s not incompetence. That’s just how humans are. The institutional memory fades, the people who lived through the crisis die off, and a new generation convinces itself that this time will be different.

That’s the whole lesson. It’s not that hard money is morally superior to paper money. It’s that hard money is the only form of money a government cannot debase. Once you remove that constraint, the long-run outcome across every civilization we have records for is the same: eventual debasement, eventual crisis, eventual restructuring.

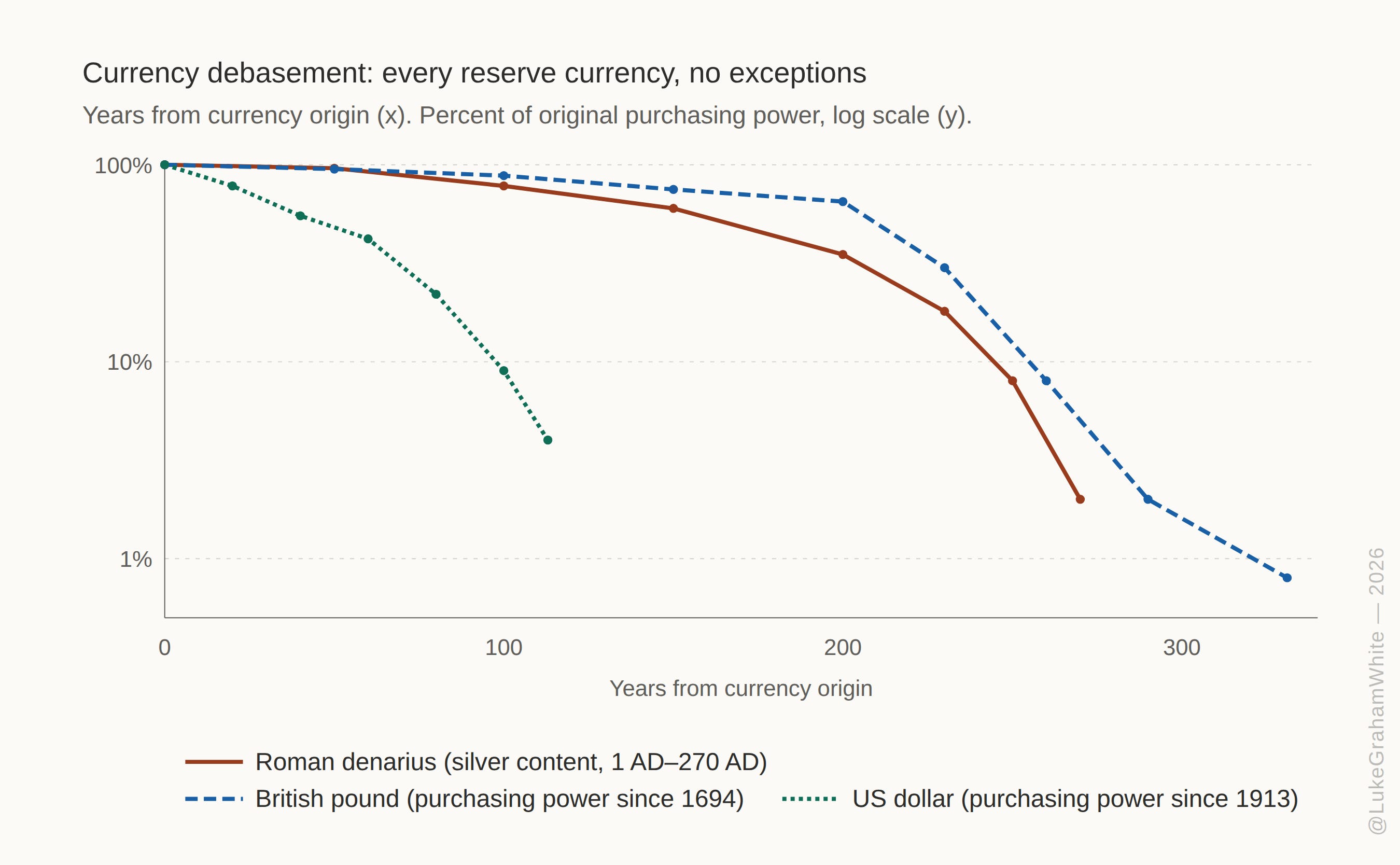

Three empires, three reserve currencies, the same trajectory.

The Roman denarius lost 98% of its silver content over three centuries. The British pound has lost more than 99% of its purchasing power since the Bank of England was founded in 1694. The U.S. dollar has lost something like 96% of its purchasing power since the Federal Reserve was created in 1913. None of these were accidents. They were choices, made gradually, for reasons that seemed reasonable at the time.

And those are the slow versions — the empire-grade decay across centuries. The faster versions are uglier, and they happen when the political constraints come off all at once.

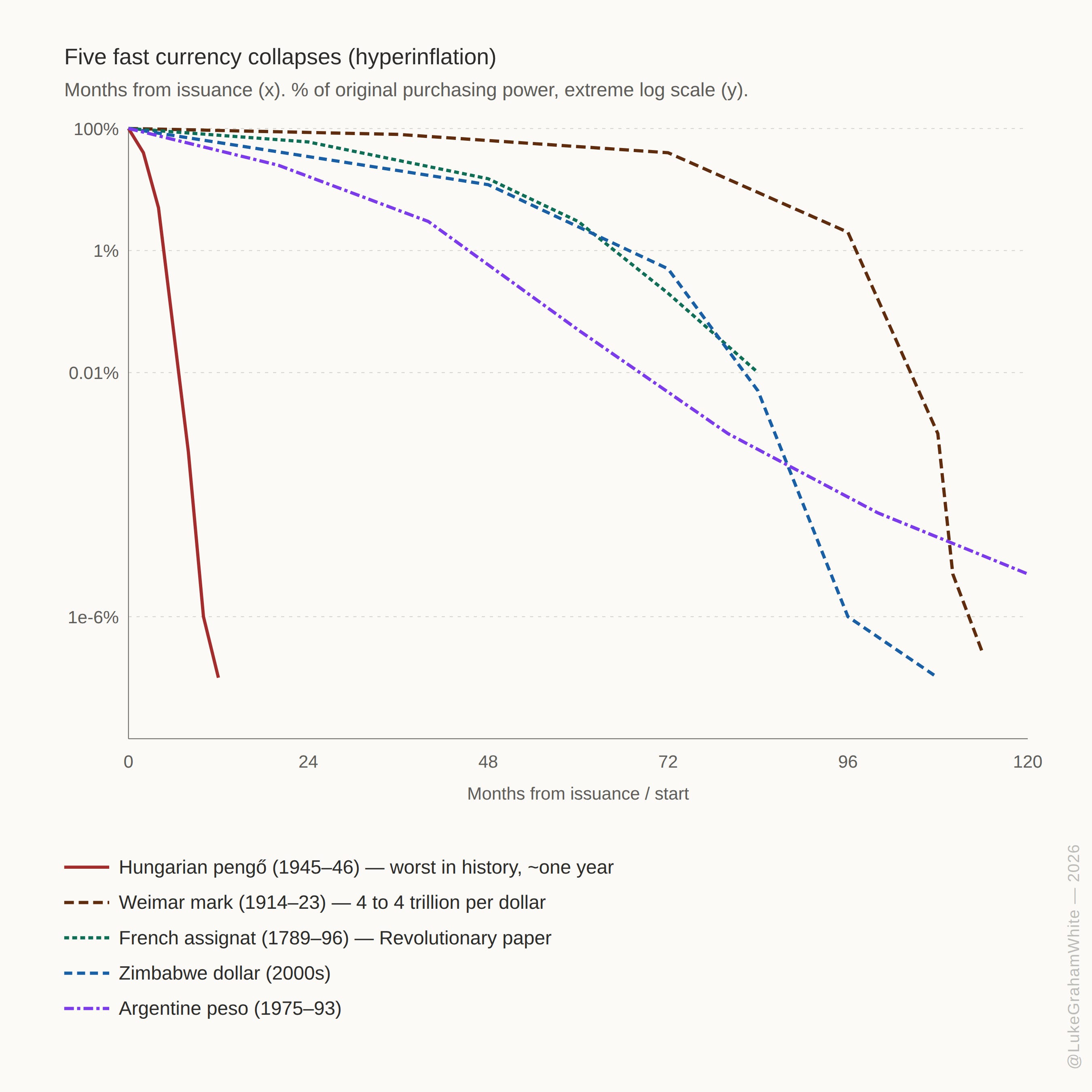

Five fast collapses on a single log axis. The Hungarian pengő fell to one ten-millionth of one percent of its original purchasing power in roughly twelve months.

These are the cases the textbooks remember. The Hungarian pengő — the worst hyperinflation in human history, completed in about a year. The Weimar mark, where four marks bought a dollar in 1914 and four trillion marks bought a dollar in late 1923. The French assignat, born of the Revolution, dead within seven years. The Zimbabwe dollar of the 2000s, the Argentine peso of the late 20th century, and dozens more we don’t have time to chart. The fast collapses look different on the page but they share the same architecture: a sovereign with a printing press, a fiscal hole that can’t be closed politically, and the belief — always the belief — that this time it’ll be controlled.

Now flip the coin. The other way late-cycle debt regimes resolve is the opposite failure mode — not the currency dying, but the assets dying. A balance-sheet recession where credit contracts faster than the central bank can reflate it, debts get repaid in the worst possible kind of dollar (the appreciating one), forced selling cascades through every leveraged book, and prices collapse across stocks, real estate, and potentially even commodities at the same time. Cash and short-duration government debt outperform everything. This is what most people who haven’t lived through one think a “crash” actually is. The textbook examples are sobering.

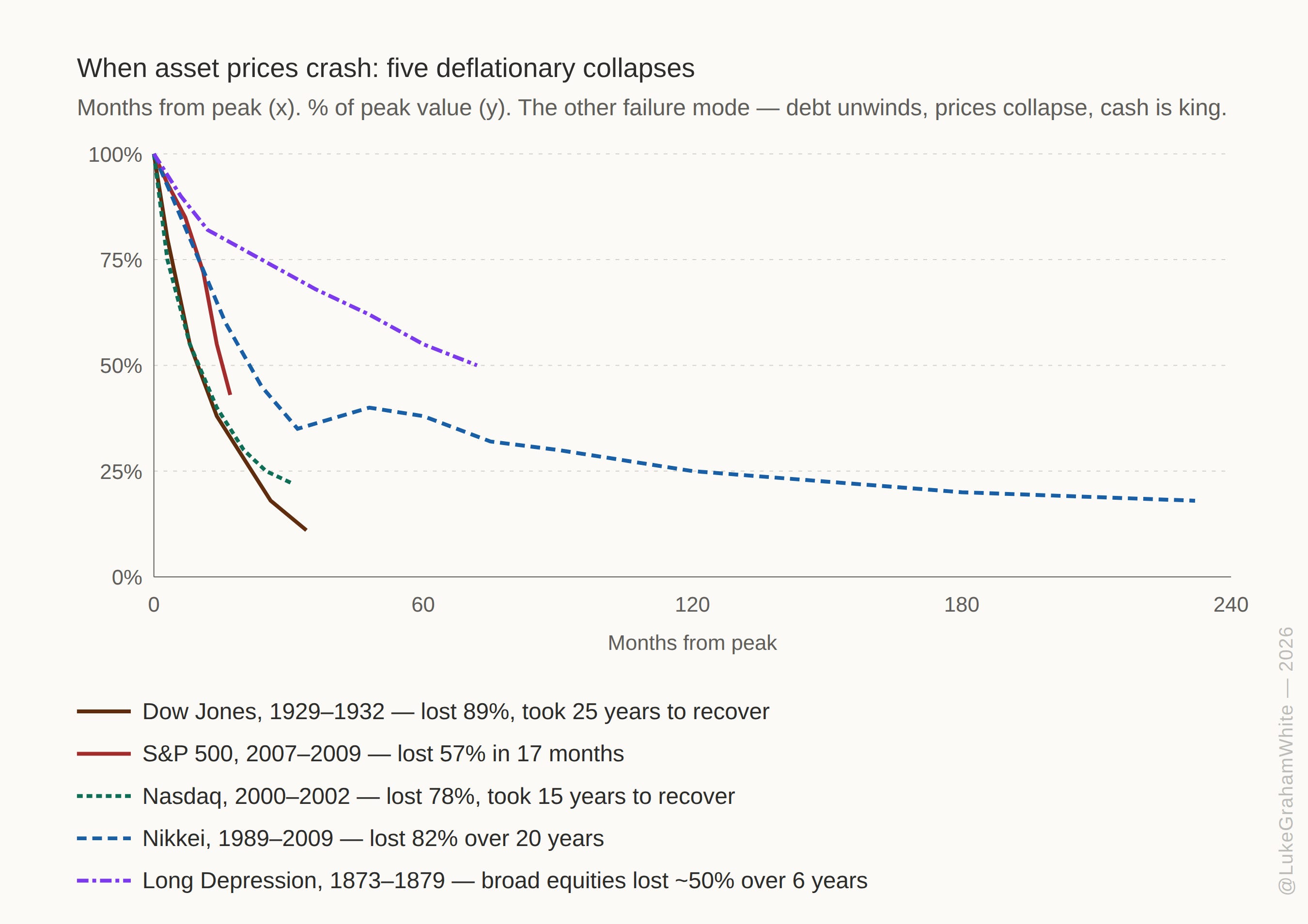

Five deflationary collapses, all measured as percent of peak. These are the cases where the assets die instead of the currency.

These are not exotic. The Dow lost 89% of its value between 1929 and 1932 and didn’t recover its 1929 peak in nominal terms until 1954 — a quarter-century of pain. The Nikkei peaked in December 1989 at almost 39,000 and bottomed twenty years later at around 7,000, a generational drawdown that defined modern Japan. The Nasdaq lost 78% from 2000 to 2002, and the index didn’t reclaim its dot-com peak until 2015 — fifteen years. The S&P 500 lost 57% in seventeen months during the GFC. The Long Depression of the 1870s shaved roughly half off broad U.S. equities over six grinding years. Different eras, different catalysts, same architecture: leverage built up over a long expansion, then unwound at brutal speed once the music stopped.

Why both charts? Because the late-cycle resolution path is genuinely uncertain — and historically, both have happened. Sometimes the political pressure to print wins (Weimar, Argentina, Zimbabwe) and you get hyperinflation. Sometimes the political pressure to defend the currency wins (1929 America under Hoover, 1990s Japan) and you get deflation. Sometimes the regime tries to do both at different times and gets sequential versions of each. The thing that’s almost never on the menu is “resolution without pain.” That option got priced out of the future when the debt got too big.

The Roadmap: What the Rest of This Year Looks Like

So let me try to sketch what I think is likely between now and the end of the year, with the obvious caveat that predictions are worth what you pay for them. But if you accept that this is all probabilistic and cyclical, the base case becomes easier to describe.

First, we’re probably already at the threshold of recession, or right on the edge. Henrik Zeberg’s business cycle model — which has identified every U.S. recession since 1950 — is the cleanest read on this I’ve seen. His Leading Index broke below equilibrium in November 2024 (his “iceberg moment” — the structural damage is done). His Imminent Recession Indicators are clustering as of early 2026, behavior consistent with late-slowdown tipping-point dynamics. The Coincident Index is approaching its threshold but hasn’t crossed yet — the ship is taking on water but isn’t officially sinking. The labor market is the cleanest tell: the 12-month moving average of nonfarm payrolls has dropped below the levels that historically precede every recession since the 1970s, with October 2025 revised to a loss of 173,000 jobs and the months since hovering around the flatline (plus let’s be honest these numbers are JUICED). The 10Y/3M yield curve has uninverted from a deep inversion — the same trajectory that preceded 1990, 2001, and 2008 by months, not quarters. None of this is a guarantee. But it’s the shape of a late-cycle economy that is closing in on the transition. Expect the official recession call to come retroactively, as it always does.

Second, the Fed will be caught in a vice. This is Dalio’s exact scenario. If they hold rates to fight sticky inflation, they crush the housing market, small businesses, and anyone with floating-rate debt. If they cut aggressively to bail out the economy, inflation comes right back — because the underlying problem is fiscal, not monetary. They’ll probably try to split the difference and satisfy no one. We will write about the Fed’s uselessness later on in detail.

Third, the Treasury’s financing problem gets louder. The U.S. is running deficits around 6-7% of GDP during peacetime, at full employment. Interest expense now exceeds defense spending. The only way this math works out without either a severe fiscal contraction or a debt restructuring is inflation — slow, steady, politically manageable inflation that erodes the real value of the debt over a decade or two. That’s the path of least resistance, and it’s the one we’re already walking.

Fourth, real assets should continue to outperform — but with a critical caveat. Gold has been making new highs. Real estate, productive businesses that throw off real cash flow, commodities — these are the things that historically held value through late-cycle periods. Over the full arc of a Big Debt Cycle, the paper promises lose value and the tangible, scarce, productive things hold or gain. That’s the structural call.

Bitcoin is the more interesting case, and a quick note here because I have a lot more to say about it elsewhere. The short version: Bitcoin is a risk asset right now and it has to prove itself before it earns the safe-haven label. It was born out of the GFC, but it has never actually lived through one as an asset class. Every drawdown it’s seen — including the 2022 crypto-internal deleveraging — has happened inside the most liquidity-abundant regime in history. The 2008-style margin-call event, where every risk asset gets sold indiscriminately and only gold, treasuries, and cash hold up, is the test BTC has not yet passed. If it’s what its strongest proponents say it is, it’ll pass. But until then, treat it like a high-beta risk asset with safe-haven plumbing. Position size accordingly.

If you want the full version of this argument — including why I think Saylor’s conviction is real but cannot be your timing signal — read my prior piece, “Everyone Is Right. Everyone Is Early.” That’s where I lay out the BTC structure for this cycle, the ETH asymmetry, and the position-sizing framework I actually trade.

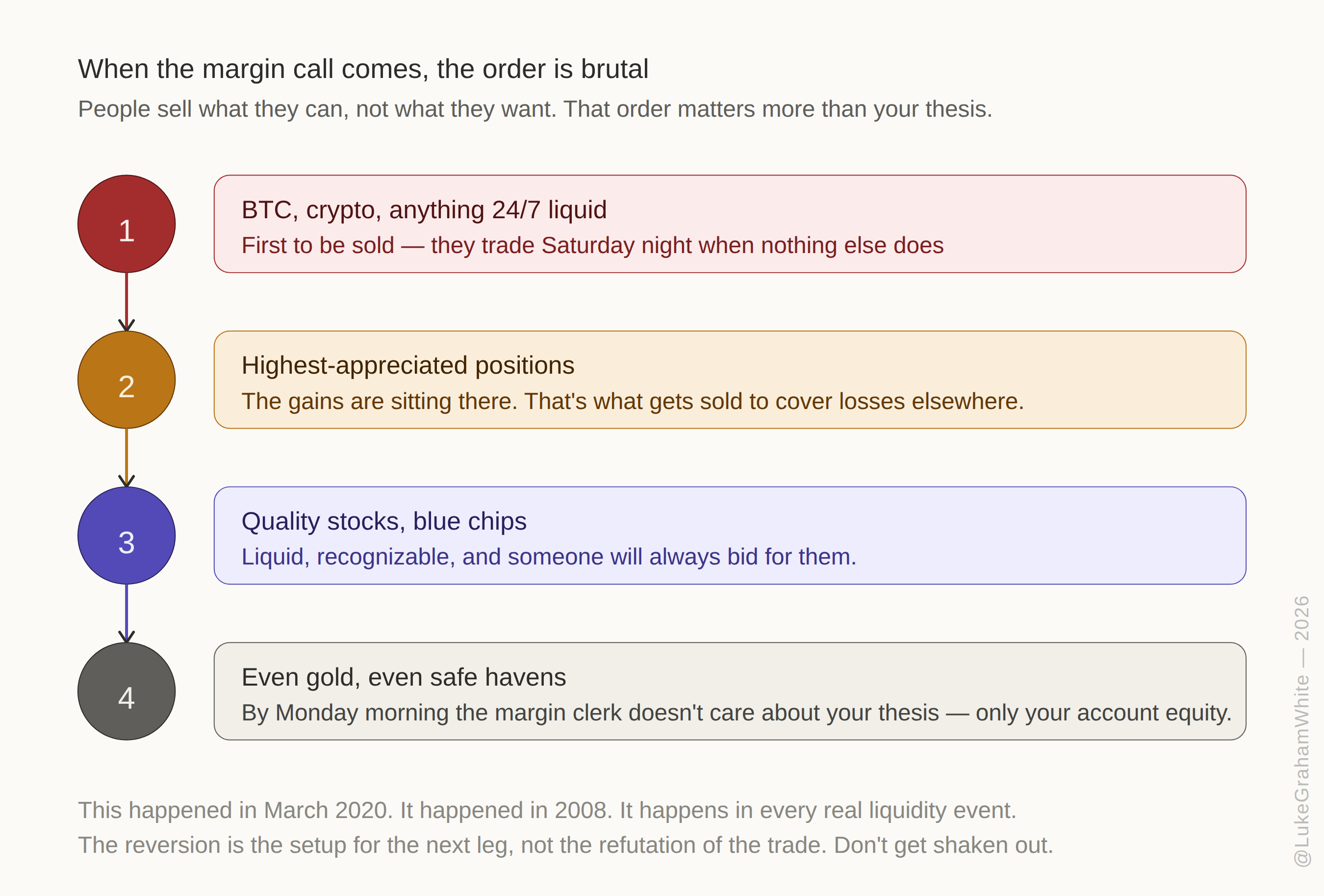

Here’s the part most people miss, and it’s the part you only really learn by living through a liquidity event: in the acute phase of a late-stage debt cycle, everything reverts at once. When the margin calls start coming, people sell whatever they can, not whatever they want. That order matters.

The order of forced selling in a real liquidity event.

The first things to get hit are the riskiest assets that trade 24/7 — Bitcoin and the rest of crypto sit right at the front of that line, precisely because they’re liquid on a Saturday night when nothing else is. Then it moves to whatever has appreciated the most, because that’s where the gains are sitting and that’s what gets sold to cover the losses elsewhere. Gold gets sold. Quality stocks get sold. Even the assets that should hold value get sold, because the margin clerk doesn’t care about your thesis — they care about your account equity by Monday morning.

This happened in March 2020. It happened in 2008. It happens in every real liquidity event. The same assets that you want to own for the next decade are often the ones that get crushed hardest in the panic that precedes the recovery. So the structural call and the tactical call can look like opposites for a few weeks. Be ready for that. Don’t get shaken out at the bottom of a forced-selling cascade thinking your thesis was wrong. The reversion is the setup for the next leg, not the refutation of the trade.

Fifth, expect the political temperature to keep climbing. This is Strauss and Howe’s territory. Fourth Turnings are when societies reinvent their institutions through conflict. It can be ugly, but it’s also when real change becomes possible after decades of incremental drift. Some of what looks like chaos is actually the precondition for the next High.

What to Do With Any of This

I’ll close with what I’ve actually come to believe after almost twenty years of trying to figure this stuff out, starting from the wreckage of 2008.

The first thing is that the single biggest edge any individual has is the willingness to zoom out. Most people are trapped inside the news cycle, reacting to whatever’s in front of them. If you can train yourself to read history, to think in decades instead of weeks, to recognize the patterns that keep repeating — you are operating on a timescale that almost nobody else is. That alone is worth more than any specific trade or position.

The second thing is to own scarce, productive assets. Not promises of things, not pieces of paper that represent things — actual things. Equity in real businesses. Real estate that produces cash flow. Commodities and hard money. A skill that generates income independent of any employer. Every single one of the defaults Reinhart and Rogoff catalog wiped out the people holding paper. The people holding productive, scarce assets generally came through. AI has given every single person on this planet the ability to learn to do something new. Don’t forget this is massive opportunity — and you can be interacting with AI instead of doomscrolling on your phone.

The third thing is to keep some hard money. Whether that’s gold, silver, Bitcoin, or some mix, having a slice of your wealth in a form the government cannot print is historically the single most reliable hedge against the endgame of a long debt cycle. You don’t need to go all-in. You just need to not be caught flat-footed.

And the fourth thing is to take the long view. This is not the end of anything. It’s the end of one cycle and the beginning of the next. The last Fourth Turning gave us the worst depression and worst war in modern history — and then the longest period of peace and prosperity the country has ever seen. The question is just what you’re positioning for, and whether you’ve done the work to recognize where we are on the map.

LOOK TO MY COMING AT FIRST LIGHT ON FIFTH DAY. AT DAWN, LOOK TO THE EAST.

The Rohirrim always come.

Further reading:

Ray Dalio — Principles for Dealing with the Changing World Order and How Countries Go Broke: The Big Cycle

W.D. Gann — Truth of the Stock Tape (1923), Tunnel Thru the Air (1927), and the 1929 Annual Forecast (still in print as a reprint)

William Strauss & Neil Howe — The Fourth Turning (1997) and Howe’s The Fourth Turning Is Here (2023)

Carmen Reinhart & Kenneth Rogoff — This Time Is Different: Eight Centuries of Financial Folly

I enjoyed your article too, full of insights and detailed thinking process. Thank you for generosity of sharing your wisdom via hard experience.

Excellent article 👏🏼 thank you ☺️